Abstract

Financial institutions have spent millions (if not billions) on owning and retaining customers, measuring their share of a customer wallet and LTV as components of overall business value. Blockchain (Web3) is now democratising financial relationships and making it possible to separate true ownership of money from the experience of using it.

In short, this means that customers can pick and choose light touch platforms that fit them best. They are truly empowered to quickly adopt new, exciting services as they are built. It means competition can flourish, but also that these new services must be lean and laser focussed on their own customer value proposition.

Customer loyalty is waning, they’re expecting more, and if you’re having to spend up large to acquire (and wait years for payback) you’d better have big pockets.

Introduction

The ethereal concept of a neo bank has come up often in my life with bankers, techies and payments gurus. We have seen the huge customer growth of UK stalwarts Monzo and Revolut as well as 86400, Up, Judo, to name a few in Australia. In my home of New Zealand, as of now there is no credible upstart and we can point to a few reasons, but number one must be the limited TAM in a country with just 5m people (as of October 2021) and a corresponding risk/reward difference to larger markets. It makes sense to build globally rather than focus just on our little country.

On that point, NZ is well placed to overachieve in the next round of financial innovation as we do not domestically have the deep pocketed ecosystem required for blind customer growth.

We have cross border access to global products, particularly from the UK and Australia. The UK players are well entrenched, coming out of a thriving fintech ecosystem where there is cash to burn. The Australian cohort seems well aligned with registered Banks given the regulatory environment there.

Core financial services is a tough industry to break into, and you need time and money to do it and it could just be a simple waste of time. Time and money are pretty big moats with some dangers also lurking in the moat in the form of regulation and competition.

What the at-scale fintechs have done really well is pushed the incumbent financial institutions and banks to provide better UX, talk in sprints, squads and really try to clear the cobwebs off their tried and often tired infrastructure. I like what Wise (previously Transferwise) have done, and they are profitable after many years operating. They are arguably an exception.

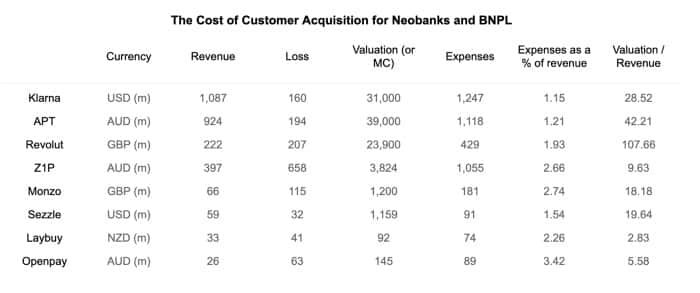

Most of these fintechs have however struggled thus far to convert their massive customer growth into solid, enduring business models.

- Monzo: ~£115m annual losses on Revenue £66m for a £1.2b valuation

source: https://sifted.eu/articles/monzo-annual-results-2021/ - Revolut: £207m annual losses on Revenue of £222m for a £23.9b valuation

source: https://techcrunch.com/2021/07/15/revolut-confirms-a-fresh-800m-in-funding-at-a-33b-valuation-to-supercharge-its-financial-services-superapp/#:~:text=As%20a%20further%20point%20of,million%20%28%C2%A3166%20million%29.

Or a summary of various Neobanks and BNPL players sorted by revenue (note: this information will become obsolete, fast);

So it’s pretty clear that these are not businesses with tried and true profit generation (aside: just let me clarify that this is OK if the shareholders believe in management’s vision and have faith in their execution capability).

At its root, these amounts are spent in the hope of increasing LTV to a level where shareholders can get their money back. They are spending it to gain custody of the customer for the medium/long term, and their hefty valuations rely on it.

An investment thesis reliant on someone else being willing to take the loss making asset off your hands for a higher price faces an expiry date at some point. It has its place, definitely, but requires investors and management alike to agree on what the plan is. Ownership, or loyalty of the customer is paramount for success under this model.

It’s about scaling as fast as possible and spending money to do so (think Reid Hoffman’s Blitzscaling).

I haven’t seen a fintech yet go ‘hey, let’s stop spending ahead of future forecasted growth and just farm the customers we have’. What happens if the future forecasted growth doesn’t come? What if technology, or trends start reducing YoY growth before this happens? What happens if customers now don’t want to give you the data you need to maximise LTV? It feels a bit like some are paying up large for customer acquisition, compensating for the fact that there might not be an entirely natural or valuable product market fit.

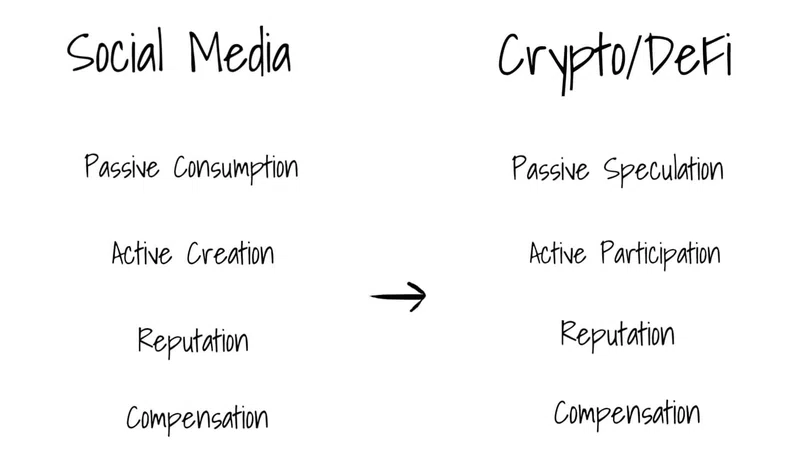

Specifically the CAC/Payback model focusses hard on LTV, holding loyalty of the customer for as long as possible, combining personal data and scale to bring future profits. It relies on 1on1 deep relationships, trust and future new products within the fintech’s ecosystem to scale into a sustainable, profitable customer base and subsequent business model.

This is how banks operate also, although they are at the maturity stage. The walled model is tough for competition, and ultimately worse for the customer. It stifles innovation, as every new product-led business needs to start from one line of code. It takes time and needs cash. There has been no easy way to leverage customer-owned data and build light touch offerings on top of it.

But this appears to be changing.

How can Blockchain impact user experience in light of this?

I believe that the way customers use financial services is going to change significantly.

Customers are less loyal. Right now, they have multiple providers for most non-bank financial needs. I know many people with Wise, Monzo, Revolut cards in their wallet (at the very least). They will have multiple BNPL cards.

In blockchain, cryptocurrencies and the Web3 world there is a different approach.

Platforms and entire value chains are being created with a single sign on (usually using Metamask, a browser extension) where their ledger of transactions and balances of ‘funds’ are carried into each experience from a shared place.

It’s as if when you switched banks you took all of your personal financial data, and balances seamlessly across to the new one.

This is true bank-like portability and where I see a huge opportunity for fast, light touched innovators to create amazing experiences.

Now, in New Zealand I feel the time for a Web 2.0 neo-bank challenger has passed. But excitingly, new blockchains (eg SOL) or Ethereum Layer 2s (eg Polygon, METIS) are starting to bring latency and transaction costs down to real world, viable levels. As these ecosystems gain the confidence of users they will spawn more innovative, light touch and ultimately customer driven financial experiences.

What Next?

There are some key points touched upon here to unravel in future articles:

- Existing payment infrastructure, the incumbents

- Light touch apps already built upon non-custodial wallets

- Core themes from my own introduction to blockchain

- Merging existing infrastructure with Web3 wallets in a transitionary way

Reach out to me if you like what you’ve read or would like me to delve deeper in to a specific topic in future articles. Let’s keep the conversation going.