These days, as a Research Team Lead of Skkrypto, a Blockchain Network of Sungkyunkwan Univerity, I am interviewing new applicants. Many applicants said that the recent rapid growth of DeFi made them interested in Blockchain. Moreover, they mentioned that they believe DeFi (and also Blockchain) will threaten traditional banking services and trigger disruptive innovations. This is the perception of the public regards to the relationship between Blockchain and Banking — Substitutes, not Complements. Of course, this is not a surprising result.

Decentralization, one of the most significant features of Blockchain, is the primary reason for this misperception. The public believes that Blockchain will enable transactions without any centralized institutions. However, there are still many things centralized institutions can do with Blockchain, and, of course, vice versa.

Blockchain within Banking: Improving Internal Process and Transaction

Blockchain innovates the traditional banking system in two aspects — internal and external aspects. Regarding the internal aspect, blockchain can trim Know-Your-Customer (KYC) and Anti-Money Laundry (AML) processes, two major internal processes of banking. Moreover, for inter-bank or international transactions, blockchain can advance them significantly.

Improving Internal Processes: KYC and AML

KYC and AML need extremely complicated validating processes to verify customers and transactions, respectively. The operations are mainly focused on acquiring and verifying related data and require much labor. Blockchain’s two significant features — distributed ledger and uneditable records — can lower inputs significantly.

The distributed ledger allows an ecosystem’s participants to share and save data individually. Validators do not have to collect all necessary data since they can easily get the data from this system. Moreover, since records on a blockchain are uneditable, validators do not have to verify additionally and can significantly reduce labor inputs.

COOV, a COVID-19 vaccination verification system of Korea, is an excellent example of this. COOV is based on a private blockchain network and allows Koreans to verify each others’ vaccination information without concerns of the infringement of privacy. Please refer to this website for more details: https://ncv.kdca.go.kr/menu.es?mid=a12507000000

By converting the subject information of COOV, vaccination information, to financial information, financial institutes can easily build efficient KYC and AML processes and will be able to invest the saved inputs to create more value for customers.

Improving External Transactions: Foreign Transfer and Payments

Decentralization is the most significant feature of blockchain and enables transactions without accompanying brokers, such as payments companies or middle banks. Thanks to decentralization, participants can enjoy lower fees and faster transaction time. Transfers via blockchain are getting more popular — e.g., from 2020 to 2021 Q3, transaction volume via Ripple grew by 100%. Some people believe that this shows why DeFi and crypto will threaten traditional banking services, but I disagree.

Currently (and until crypto becomes a primary medium of exchange), fiat currencies are still acting as the medium of exchange, and final customers must convert their crypto to fiat on CEX by paying additional fees. Therefore, the current economic system still needs banks as the last processors, and it implies that banks can provide more efficient services for their final customers by taking blockchain transfer systems. Furthermore, payments processing systems based on blockchain will allow transactions without processors, such as VAN or credit services.

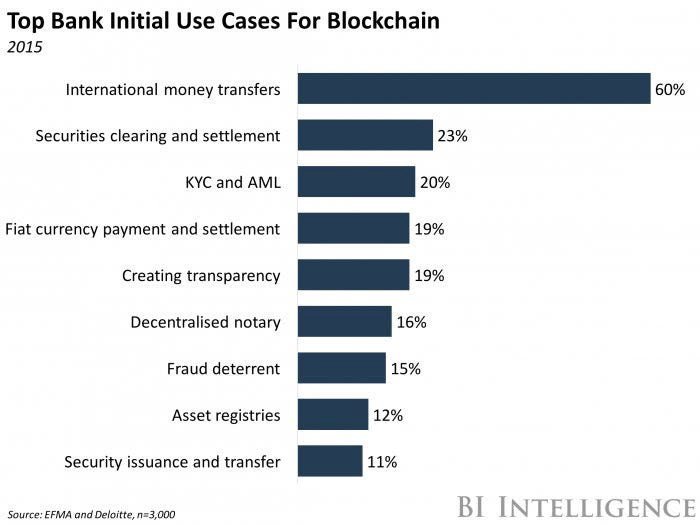

Also, there are many other segments in banking that blockchain can improve:

image source: Here’s how banks can save big with blockchain, Business Insider, https://www.businessinsider.com/heres-how-banks-can-save-big-with-blockchain-2017-1

Banking within Blockchain: Stabilizing Blockchain Ecosystem

Blockchain services also need traditional banking systems, either. Blockchain is based on autonomy and anonymity. This characteristic leads to a serious concern — no one is responsible for the ecosystem. Although many blockchain-based services have their own governance systems, many threats and problems regarding regulation and risk mitigation still exist.

Blockchain-based services, especially DeFi services, lack essential processes for the financial ecosystems, such as KYC and AML. Of course, KYC and AML will hinder the system’s anonymity, but to be included in the real world and widen the ecosystem, following current regulations is necessary. For this, the traditional banking services’ internal control processes will be helpful.

Banking services can help blockchain services in terms of risk mitigation. The risk mitigation system includes various aspects, from internal control to investment diversification. DeFi services did not face any severe financial crisis and did not have opportunities to develop these systems. Adopting banks’ risk mitigation processes will help them build the system efficiently and effectively.

As I stated, I believe that banking and blockchain are complements, not substitutes, and can create more significant value together. Moreover, for the upcoming Metaverse world, the combination of banking and blockchain will lead the disruptive innovation.