Today’s bank customer expects (hyper-)personalized advise (the "It’s all about me" trend), i.e. he expects to get advice, which is completely tailored to his specific needs of that specific moment.

At the same time, banks are forced to cut costs, meaning 1 front-office bank employee is expected to service more customers than ever before. Automating tasks is the solution to increase the productivity of bank employees, but in order to keep IT complexity acceptable, automation usually comes with simplification and standardization of processes. These 2 evolutions seem contradictory. AI models are considered to be the answer to resolve this dilemma, but these techniques are not fully mature yet. Furthermore AI models often mean that bankers have less control on the expected outcome, which in case of financial advice is not desired by the bank and usually also not desired (or even not allowed) by regulators. Regulators want to make sure that financial advice is always appropriate and suitable for a customer, which is difficult to prove with an AI model you cannot fully explain.

One other solution to this dilemma, which is not that common yet, is so-called crowdsourcing, i.e. involving the crowd or in this case the bank’s own customer base. Already today simple tasks are executed by using the power of the crowd. Typical examples are the classification of transactions in financial budget tools, the training of AI models (e.g. classification of pictures via so-called mechanical turks like Amazon Mechanical Turk, Clickworker, Microtask, CloudCrowd, RapidWorkers, Samasource…), idea generation (e.g. LEGO Ideas platform or PepsiCo’s "Do Us a Flavor" campaign…), completing digital maps by contributing with pictures (e.g. Mapillary), content creation and review (e.g. Wikipedia)…

This idea could also be explored for financial advice in general and more specifically for investment advice.

Also in the investments domain, the general trend is to provide more individualized investment advice, i.e. guiding the customer in his investment decisions and providing a continuous follow-up of his investment portfolio.

This consists of a number of tasks:

- Guiding the customer in initiating his investments by

- Defining new triggers for launching an investment, like rounding debit transactions and automatically investing the rounding difference, automated investment plans investing a pre-defined amount on a regular basis, PFM tools proposing to automatically invest excess cash…

- Recommending investments based on the customer’s profile, i.e. both his risk profile, but also his preferences like SRRI or cultural/religious preferences. So-called Robo-advisors provide a solution to this. Cfr. my blog Digital Investment Advice - Should Financial Advisors start looking for another job? (https://bankloch.blogspot.com/2020/02/digital-investment-advice-should.html) for more info on this.

- Guiding the customer into an optimal risk management, i.e. helping the customer to maximize his portfolio diversification, to create automatic stop-loss orders or limit-orders in order to respectively limit losses or take profit in time and hedging certain positions via derivatives used in a hedging capacity (cfr. Capilever’s RSTT product - https://www.capilever.com/rstt/)

- Follow-up the investment portfolio by:

- Continuously checking if the portfolio is still in line with the risk profile and investment constraints and is still sufficiently diversified.

- Automatic rebalancing of the portfolio to fit a model portfolio or recommendation strategy

- Notify the customer about certain events, like a position having reached X% profit or loss, a position on which a corporate action has been announced or has occurred, a position reaching certain lower/upper threshold on volatility, a maximum exposure in a specific sector/region/currency/issuer reached…

- Push certain info to the user in the form of alerts and suggestions (via mail, SMS or mobile app push notifications)

- Detailed reporting of the current investment portfolio, like different exposure views (currency, sector, issuer, country/region, asset class, risk level…), detailed performance views (portfolio performance, position performance and performance attribution), risk views (like portfolio and position VaR, risk-adjusted return…) or cash-flow forecasting (i.e. what are the expected income flows in the form of coupons, dividends or reimbursements)

See also blog "Investing – A spectrum of choices" (https://www.capilever.com/blog-18/) for more info on this.

Usually all this is done by digitizing the portfolio management processes and by combining (a so-called hybrid model) a fully digital robo-advisor with the expertise and personal touch of an investment advisor (which can support a high number of customers as they are supported by excellent tooling).

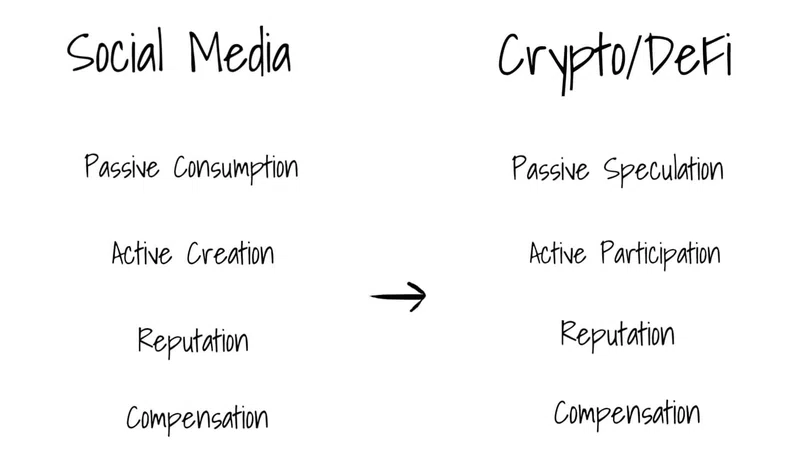

However crowdsourcing can also be a solution to this problem, i.e. crowdsourcing in the form of social trading networks, where the investment expertise of the crowd (i.e. of other investing bank customers) is leveraged. I already described such a concept for a socially managed investment fund (cfr. my blog "The idea of a collaborative investment fund" - https://www.fintechna.com/articles/the-idea-of-a-collaborative-investment-fund/), but obviously the same technique can also be used for individual investment portfolios.

The most known example of such a social trading network is the Israelian company eToro, but other platforms exist as well, like NAGA Trader, ZuluTrade or Darwinex.

Such platforms offer next to the traditional trading and portfolio management features, following "social trading" functionalities:

- Express your own investment preferences & securities knowledge/interests (i.e. create your social profile)

- Search and follow other investors/traders, e.g. list of Top Traders and Rising Traders

- Receive recommendations of other investors with similar preferences ("Find People Like Me")

- Connect and communicate with other investors

- Rate other investors (in different categories, like clarity of advise, willingness to help, investment performance, stability, risk level, ethical rating…)

- Search and consume content published by other investors and rate it (e.g. via "Like" button). Like in other social media platforms an engine should push the most relevant info in your feed. This info can be posts from other investors (you are linked to or that you follow), but also public market news/insights (e.g. analytics on companies, annual reports, presence of company in the media…).

- Share your own investment insights, strategies and experiences, e.g. tips and tricks, but also fundamental and technical analyses of specific securities and/or companies

- Monetise your content publications (advice & analyses) or monetise your own trades by allowing other customers to copy your portfolio (Earn Copy Bonus)

- Request an analysis of your portfolio to a specific investor or to the crowd

- Track portfolio of another investor, i.e. automatic mirroring/copying (= auto-copy) of investment portfolio by following trades with a fixed investment or by copying their trades in percentages.

- Join investment games to win prices with investing with virtual portfolio

Till now such platforms are offered solely by specialized Fintech companies, but it would be wise for incumbent banks to also dive into this, as it could not only increase customer engagement (and retention), but also reduce operational costs, as it allows to scale personalized investment advice, without the associated cost increase (for hiring extra investment advisors).