Abstract of the "From Risk Transfer to Risk Prevention" paper by Isabelle Flückiger - Director New Technologies and Data at The Geneva Association - and Matteo Carbone - director of the IOT Insurance Observatory and board member of Net Insurance,

The Internet of Things in insurance

Risk prevention is inherent to insurance. Recent developments in technology and the corresponding availability of data, however, have the potential to influence change in this space. A key driver of this development is the Internet of Things (IoT), the growing network of connected devices ranging from consumer wearables to industrial control systems.

IoT usage is maturing in both corporate and consumer businesses. Indeed, the adoption of IoT by all industries is steadily growing, and according to a recent report by Kaspersky, 61% of enterprises already use IoT applications. So, nearly two thirds of insurers’ corporate customers have IoT applications in place, and can potentially integrate the data into insurance services.

The hyperconnection between people, machines and organisations is a prevalent megatrend seen at almost all levels of society and around the world. A recent study by Aviva revealed that the number of internet-enabled devices in the average U.K. home has increased by 26% in the last three years to over 10 devices.

Insurance IoT is a new paradigm that impacts strategy, business cases and models, and technical and leadership capabilities along the insurance value chain and in the societal risk landscape at large.

In many cases, the technologies behind prevention services are tried, tested and offered by other industries. One use case for the insurance industry – namely the use of IoT for risk prevention – has been clearly identified. What is still missing, however, is consensus on how to translate the use case into a sustainable business case that benefits all stakeholders, i.e. insurers, technology providers and customers. In addition, these IoT-enabled services of the insurance industry also support the transformation to the UN Sustainable Development Goals (SDGs) in several dimensions.

Two approaches to risk prevention

The reduction of risks faced by insurance customers can either be achieved directly – through real-time risk mitigation solutions – or indirectly – by promoting safe behaviours over a longer period.

Prevention services are not new in the insurance industry; for years, insurers have provided consumers with loss prevention advice and risk-engineering teams advise businesses in commercial lines. Ways to prevent risk, however, are changing. IoT allows risks to be better managed. This can be seen as the very essence of the evolution from pure risk transfer to a ‘prescribe and prevent’ scenario.

1) Real-time risk mitigation

Real-time risk mitigation results from the direct use of IoT technology and can either consist of:

- Automated actions by IoT actuators that impact the risky situation without any human intervention, like autonomous driving systems in cars, or

- A warning to trigger some kind of human intervention, such as a water leakage alert that activates an emergency repair service.

These risk mitigation actions can be triggered by the detection of three different situations:

- Missed safety tasks, such as scheduled inspection or equipment that needs preventative maintenance, or a diabetic patient who has left insulin at home or missed a blood sugar level check.

- A risky situation, such as a frozen pipe; a cold storage door that has been left open; spilled liquids on a supermarket floor; workers without adequate equipment in the workplace; unsafe lifting by an employee; a distracted driver.

- The consequences of an event that has already happened, such as a water leak; an unsafe worksite; an injury; or the failure of a patient to adhere to a treatment. A mitigation action is then initiated by the IoT system.

Real-time risk prevention is most mature in commercial lines, driven by the loss control culture present in commercial insurance. Field inspections by engineering teams are well established and enhancing this work with new technologies seems like a natural step.

A few personal auto insurers around the world have integrated real-time warnings in their telematics programs. This live feedback – from line departure warnings to alerts about upcoming risky intersections – influences driving behaviour and allows insurers to reduce expected losses.

Water leakage sensors are one of the most cited preventive services in home insurance. However, as of today, insurers have struggled to introduce approaches that generate substantial demand and a sustainable business case. Finding a sustainable business case in the smart home insurance market is challenging, but ongoing innovations should make homeowners the ultimate winners.

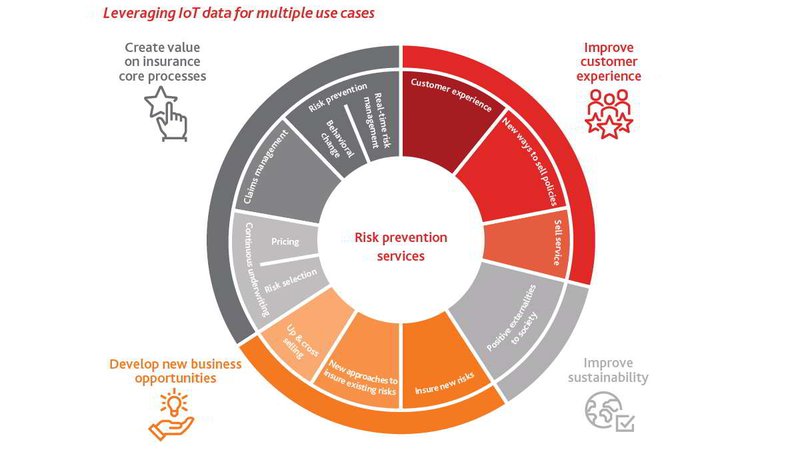

Figure 1: Leveraging IoT data for multiple use cases

Source: IoT Insurance Observatory & The Geneva Association

Bundling risk prevention with other customer services, such as security, has been the most successful approach to date. The sustainable business case is built on a bundle of different services – some sold after the purchase – and on the reduced churn rates built through customer engagement.

Life and health is the least mature field for real-time risk mitigation services. There have been many insurance pilots over the past few years around early detection, care optimisation and medication adherence but only a few examples have scaled to market level. Reasons for the slow pace of adoption in the life and health space include:

- Health costs in most countries are not fully covered by insurers but by a public health system.

- Entering into the medical device space would mean entering into the medical regulatory field.

- Medical advice comes with significant responsibility and requires deep and specialist knowledge.

- Execution at scale needs insurers to deal with many different medical service providers.

Real-time risk prevention services and approaches to them are very heterogeneous. The only common denominator is that all successful services are based on a multi-year journey.

2) Promoting less risky behaviour

The second way to prevent risk is to encourage less risky behaviour. Insurers have a role to play in creating a positive safety culture and raising awareness in society.

We can distil a three-pillar concept from the successful examples:

- Pillar one: Create awareness of the current risk level

- Pillar two: Suggest a change in behaviour

- Pillar three: Incentivise the change in behaviour

The sustainable adoption of safer habits for the benefit of all stakeholders can only happen when all three pillars are successfully implemented.

The first two pillars are closely interlinked and depend on feedback to customers. Awareness of the current level of risk leads to the question: what change will make the activity safer? Before changing our behaviour, we need to be aware of our current behaviour.

Raising awareness of risky behaviour and identifying ways to change it are not enough. There is a need to proactively incentivise people to instigate real and sustainable changes in their behaviour through rewards.

The customer’s perception of the value of the rewards, their cultural context and frequency, and the intersection with behavioural economics are all integral. Changes in human behaviour are also instinctive; a combination of behavioural economics and gamification to engage individuals is therefore needed to help to drive behavioural change.

The most mature business line is life and health. Fully individualised suggestions and challenges are provided to customers based on the number of steps registered by their mobile phone or physical activity data from wearables.

In personal auto telematics, customers often receive a detailed analysis of their driving style via a dashboard in a mobile app. Many insurers also automatically display tips for improving the driving score, or introduce contests on specific ‘issues’ – so-called leaderboards.

In commercial lines, IoT data is being used to enhance the activities of the loss control teams and to provide periodic safety insights to risk managers and supervisors of the insured companies.

The real-life case studies on promoting safer behaviour afforded the following key findings:

- The reward system needs to be set up to reinforce positive behaviour. The reachability of the reward is key.

- There are cultural aspects to incentivisation. It is important to find compelling benefits and rewards that engage target customers. What works in one country does not necessarily work in another. The rewards must be explicit and tangible. For example, monthly cashback on fuel costs is effective, but a free weekly coffee also materially influences behaviour.

- Frequency is key. A yearly premium discount is not enough. Positive engagement must be nurtured on a short-term basis. This mechanism gives people a reason to come back to the platform.

Enablers of prevention services

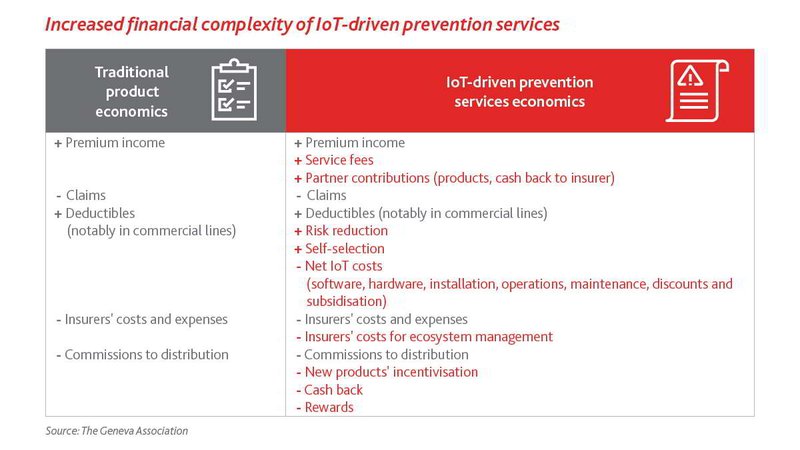

The integration of technology into prevention services greatly increases complexity. As a result, the enablers for success are the effective business transformation, cultural change and understanding of the corresponding financial management rather than the technology itself.

Figure 2: Complexity of the financial management of IoT-driven prevention services

We identified the following as the main success factors:

- C-level commitment

- Development of vision and strategy

- Development of culture and capabilities

- Finding an effective value-sharing scheme with the customer

- Management of new and complex financials

Several new elements need to be considered in the financial management of this new paradigm, such as service fees, partner contributions, self-selection effects and net IoT costs, which are harder to integrate into the economics of traditional insurance products.