Last month we had the ITC event in Vegas, and I feel obliged to dedicate this edition of the newsletter to my takeaways from this conference. It took a while to digest the two days of discussions: the first day, nine straight hours of meetings with two dinners after, eight hours of meetings the second day and other two dinners on the second one. I've honestly not yet followed up with all the people I talked with 😅

This newsletter is about facts and figures, but I'm going to offer my summary with some anecdotal evidence:

- some incumbents are getting more and more serious about innovation

- "innovators" digested that agents and brokers are here to stay

- shiny new things replaced the old ones

- everyone is trying embedding insurance somewhere.

1. Some incumbents are getting more and more serious about innovation

A few months ago, in one of the previous editions of this newsletter, I stressed my belief in the importance of insurance innovation. Well, some incumbents have come to ITC well-prepared to meet tech providers, discover new things, and exchange thoughts with their peers. This kind of incumbents - serious about innovation - had a large delegation, a shared agenda between their executives to be efficient, and even spaces to efficiently have the meetings.

Instead, some other incumbents have not shown up, or dramatically reduced their people at the event. Since insurtech stocks got hit and issues such as inflation impacted the P&Ls, the insurance incumbents that were not serious about innovation have happily and quickly canceled insurtech from their agenda.

Since the hype has vanished, we have seen those who were committed to a multiyear innovation journey, and those who were only pretending to innovate. To quote Warren Buffer - he tends to have right - "when the tide goes out do you discover who’s been swimming naked".

Instead, talking about incumbents that took innovation seriously, above a video with facts and figures about successful usages of IoT in the insurance sector. Much of these quantitative pieces of evidence come from incumbents who are members of the IoT Insurance Observatory.

2. "innovators" digested that agents and brokers are here to stay

Many (really a ton) of the tech players in the expo area were providing tools to support agents and brokers, and to help carriers to work with agents and brokers better. So it looks like the people that work in innovation (finally) get that gets and brokers are here to stay.

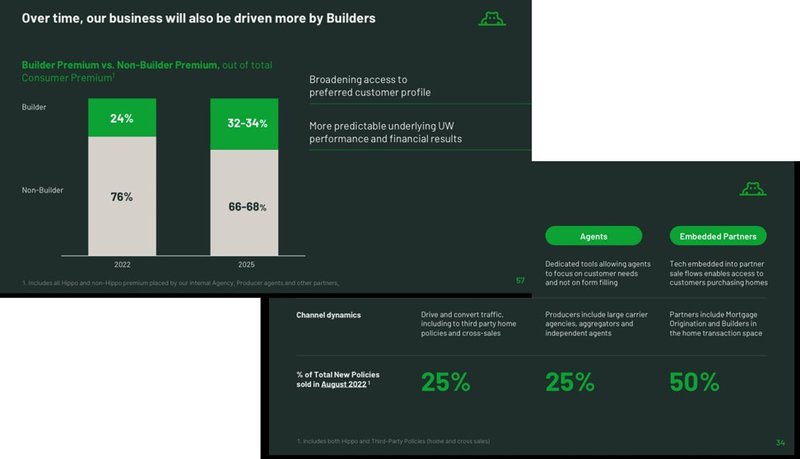

The past ITC editions were all about digital sales, DTC (direct-to-consumer) and disintermediation. I have always struggled to make people to digest that insurtech was more than D2C (and more than startups). We had tons of articles and interviews for all the pandemic period talking about the "digital shift" in the insurance sector. Even when facts and figures (as shown in the presentation below) about the premium split were available, people still pretended that the reality was different.

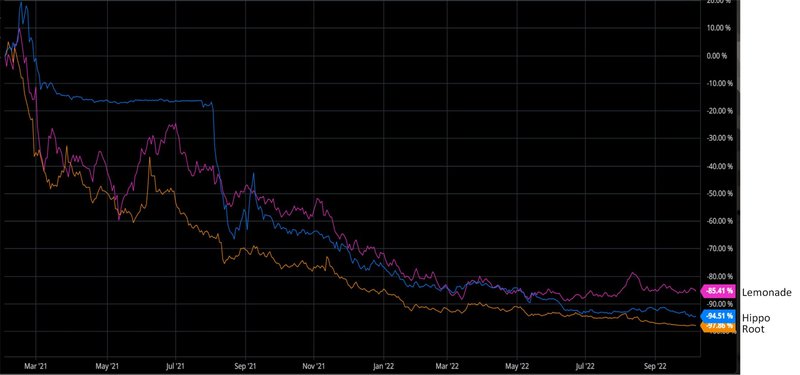

We had last year the famous trio (Lemonade, Hippo, and Root) doing a U-turn from talking s**t about agents to using them for selling more policies (or selling them with a lower acquisition cost). I commented at the time "it seems agents and brokers are not useful when you have to raise money from VCs, but they are extremely useful when you want to build an insurance portfolio!" Well, looking at the ITC floor, you can raise money even acknowledging that agents and brokers are here to stay nowadays.

Regarding U-turn, Lemonade has just done a big one (new). Many of you probably remember when they were screaming daily about how insurance incumbents were bad. Here a snapshot of a Lemonade's CEO blog post (about 6 or 7 years ago):

Last week, Lemonade announced proudly that they enter the UK market with a partnership with Aviva. Here the words of Lemonade's CEO “Pairing Lemonade’s strengths with Aviva’s promises to deliver insurance that is digitally native, yet rooted in the birth of modern statistics in the 1700s. It’s the best of both worlds, giving people a refreshing experience backed by a company they’ve known and trusted for years”.

For the few doesn't know it, Lemonade's CEO is still the same (even if the stock lost about 86% of its value from the maximum in February 2021). So, the insurance sector should be pretty proud that a "disruptor" after seven years in the sector moved:

- from believing that insurers were chronically affected by "distrust"

- to acknowledging the policyholders' trust in an incumbent insurance carrier.

3. Shiny new things replaced the old ones

Blockchain has been missed at ITC 2022. Nobody mentioned it, and I suspect someone even denied ever considering it a thing in the insurance space. Instead - in the previous ITC editions - any new venture claimed to have some blockchain within their approach...even if what was the business reason for using it were frequently unclear.

One of the shiniest new toys seems the app marketplace. I've heard about so many marketplaces in these two days in Vegas...

4. Everyone is trying to embed insurance somewhere.

Everyone - really everyone! - is trying to embed insurance somewhere. Most of the initiatives are still at a stage early enough to share only enthusiasm and big/vague expectations. Clearly, the topic is cool among the investors, and every funder is adding it to the pitch deck.

However - in order to set the expectations - a successful execution of the distribution with an embedded approach will not be enough to guarantee favorable evaluations. I described in details Hipp

o's business model and results in a past edition of the Facts & Figures Newsletter, and even more about their good performance in distributing homeowner insurance through home builders was shared on their investor day last September.

Despite these performances on the currently hot topic, their stock doesn't show any sign of recovery 👇

For a full collection of the you can look a this Jeff's post 👉 reflection posts

The week after ITC, I had the privilege to speak at the Driving the Next in motor risk organized by Swiss Re. These two days of presentations about the evolution of motor risks provided a lot of food for thought, and offered me the opportunity to exchange some thoughts with Andrea Keller and Donato Genovese.

Andrea, Donato, I've been at your conference "Driving the Next in motor risk" together with many primary carriers and players of the mobility ecosystem. Can you summarize the ambition of Swiss Re in this area, and the role of Swiss Re's telematics capabilities in this strategy?

Swiss Re is a risk knowledge company and, as such, is exploring the boundaries of risk and how it will be evolving in the future. Through the conference "Driving the Next in motor risk", the Swiss Re's Automotive and Mobility Solutions Team and the Swiss Re Institute have offered a comprehensive view on how motor risk is shifting over time from the driver to the vehicle, along the C.A.S.E. (connected, autonomous, shared and electric) trends. Swiss Re has the ambition to remain a key risk partner in the mobility space to help stakeholders ranging from insurers to car manufacturers to mobility providers succeed through those trends. Telematics was the first component of Swiss Re's strategy, with a product (Coloride) created to empower an assessment of the driver risk based on data. We now need to look also into the vehicle risk: we are supporting our clients doing so with the Swiss Re ADAS Risk Score (translating the safety technology of vehicles into actuarial terms), Swiss Re Electric Vehicle Risk Score (reflecting the peculiarities of electric vehicles in motor pricing) and Swiss Re Autonomous Vehicle Risk Assessment Framework (helping the mobility ecosystem prepare to insure a driverless future).

I've been lucky to see your team's multi-year journey in developing the current telematics mastery, and the team has shared your experience at some of the past plenary sessions of the IoT Insurance Observatory. Can you share the key milestone of this journey, the results already achieved, and the lessons learned?

At the end of 2015 we acquired a Bremen-based telematics service provider, Akquinet sls, later rebranded Movingdots; with them we started developing the telematics app Coloride, which went live in summer 2017 with the first client's customers. Since then, we have made several other launches in Europe, LatAm, US and Africa. One key lesson learnt over those years is that a user-centric approach is key in empowering a successful telematics product. The app can be a very strong and accurate one, but without proper product design aiming at adding value to the driver as well as communication strategies focusing on the key benefits for the driver, the adoption rate will be lower.

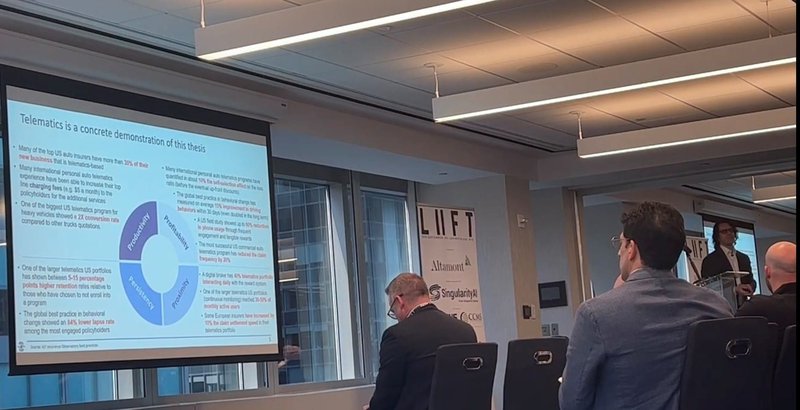

I remember your focus in improving driver safety from Andrea's contribution to the paper "From Risk Transfer to Risk Prevention". InsurTech Facts & Figures is the headline of this newsletter. Looking at the different initiatives you supported, can you share some quantitative insights about the change in driving behavior achievable in a telematics program?

Absolutely. To ensure effectiveness, our telematics solution Coloride has been developed keeping in mind behavioural economic principles, including anchoring/loss aversion, immediate gratification, social norms, framing/loss aversion/nudging, continuous engagement and reinforcement, altruism/reciprocity. The impact of behavioral interventions (coaching) to mitigate risk is very positive, with a 5% improvement of the overall driver performance after only 30 trips. More specifically, there is a 6% improvement in the speeding sub-score, 4% improvement in the distraction sub-score and 14% improvement in the manoeuvre sub-score. This improvement in driver's behavior is sustainable across clients and regions.

The international markets show entirely different levels of telematics maturity, and the characteristics of the local insurance markets require different approaches. However, what are some of the general reasons you point out to local carriers to motivate them to start their telematics journeys?

As you say, different markets show different needs. In general, we see the intention of the insurers to increase the touchpoints with the insureds as a common need. When going one level deeper, depending on the market sophistication, telematics can be used as a risk prevention tool, for customer engagement, risk pricing or cross-selling. Our client base has been interested mainly to the first two aspects; however, our solution can support a variety of business cases.