In his 2022 letter to stakeholders, Blackrock’s CEO, Larry Fink, wrote that the next thousand Unicorns won’t be search engines or social media companies, but sustainable, scalable innovators – technology start-ups that help the world decarbonise and smooth the energy transition for us all.

But, despite repeated commitments to environmental, social and governance (ESG) goals, all the evidence suggests that we are actually going backwards. Carbon emissions are expected to rebound to pre-pandemic levels, after industrial activity and levels of commuting dropped during covid. The gap between rich and poor has grown during global lockdowns, exposing even greater social divides and a gulf of opportunity. Gender and ethnic disparity remain, with women and minority groups still underrepresented in government and corporate leadership positions globally. And, as populations have grown over the past few decades, so too has consumption of natural resources and the amount of e-waste generated and not recycled.

So, what is the future of sustainable finance and where are those mythical ‘soonicorns’ to be found?

While sustainable finance – or SuFi – is still in its infancy, there are untapped opportunities at the intersection between ESG and circular business models, where finance and technology can drive a real, positive impact. This creates significant potential in four main areas, which I’ll come on to shortly, but let me start by saying how I think my own area, venture capital, can advance sustainability goals.

Being smart about how we allocate capital means we can help redress the balance in three ways. First, by developing clear ESG policies, focused on measurable outcomes. Second, by directing capital towards those companies most likely to deliver them. And third, by encouraging our own portfolio companies to measure the broader impact of their business decisions and activities and by holding executives accountable for the results. If we really drill down into the specifics of what sustainable looks like, and focus on measuring the desired outcomes, we can drive the kind of performance that’s going to tip the scale of change. Let’s use the power of the capital we invest in start-ups to create that change.

So, on to those all-important growth areas.

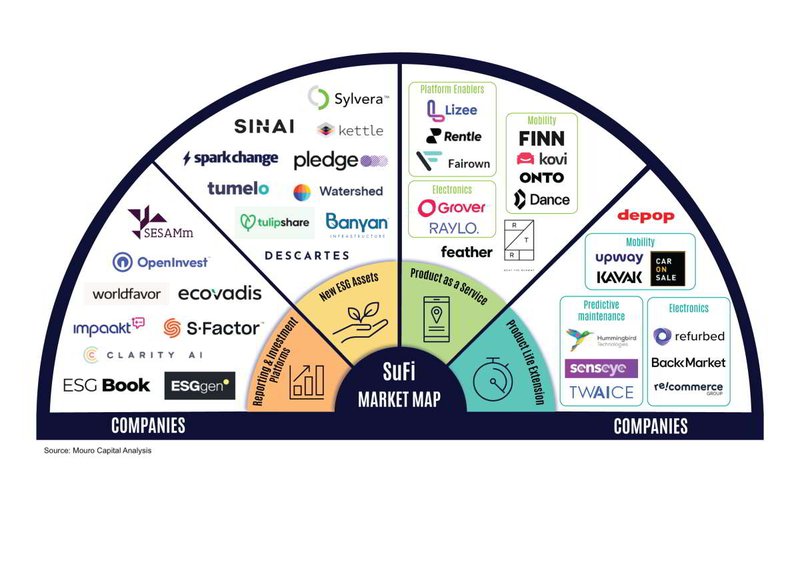

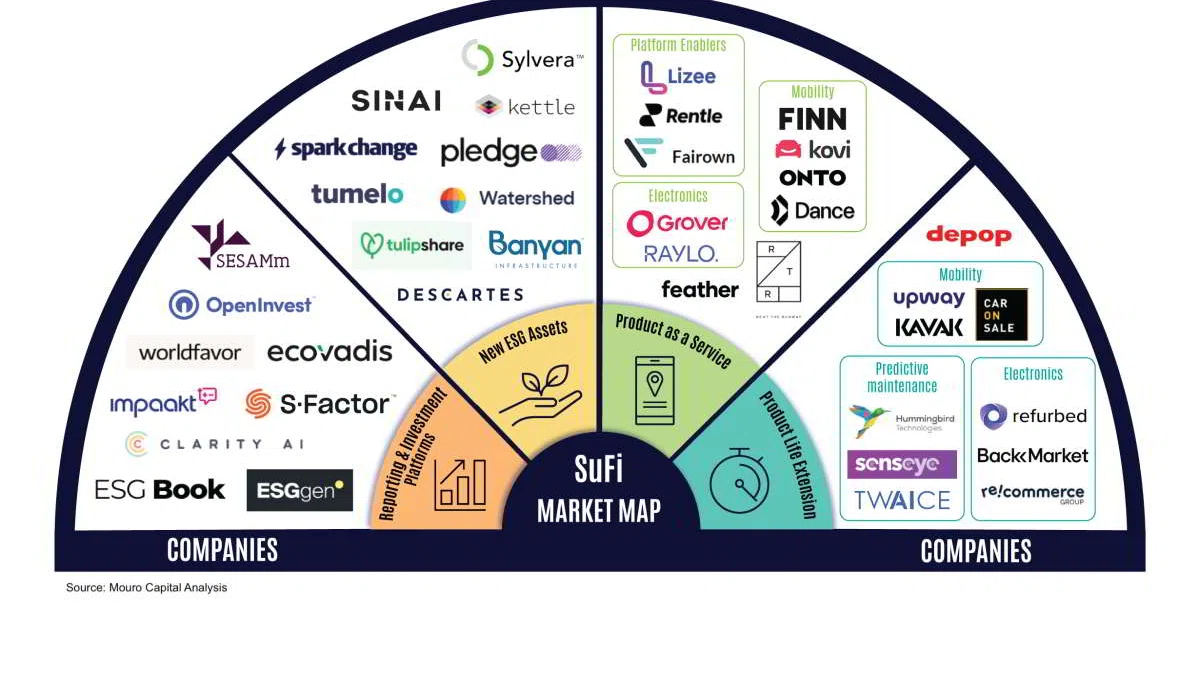

Opportunity 1: ESG platforms for reporting and investing

The frenzy in ESG compliance has triggered a need to “measure, measure, measure”, with credit agencies creating specific products, and ESG analytics start-ups mushrooming to front run the trend. Healthy streams of money have flowed to newcomers in this area but, in the absence of regulatory standards and industry-accepted practices, it is hard to identify who the ultimate winners will be. On the flip side, the ability to build trust with more accurate data and reporting will lead to improved capital allocation to companies that have a positive ESG impact.

Opportunity 2: New ESG Assets

S&P’s Global Ranking expects sustainable bonds, including green, social and sustainability linked, to exceed $1.5 trillion in 2022, up by more than 50% on 2021 and from just $200 billion in 2018 As both private and public sector players tackle their climate commitments, I expect to see further diversification and innovation in investment products, ranging from institutional and retail carbon instruments to sustainability investment platforms and marketplaces.

I would venture that soon most, if not all financial instruments (especially those traded on publicly regulated markets) will couple their traditional financial performance indicators with qualitative ESG measures. Investors will care more what drives their return, and how the nitty gritty of these securities tie in to the real economy. A key factor that has hindered wider adoption of ESG standards among the capital markets community has been

the unproven link between sustainability and financial alpha. My hope is that these new ESG assets will cast much needed light on the topic and, as a believer in the positive correlation between ESG compliance and financial performance, such positive conclusions will further boost the sector, even beyond S&P’s Global Ranking predictions.

Opportunity 3: Increasing product as a service (PaaS)

PaaS models are emerging across every industry, from automotive to IT hardware and industrial equipment. Just as with the ‘device-as-a-service’ sector, the compound annual growth rate is expected to hit 38% from 2021-25, reaching more than €476 billion globally.

The model helps reduce environmental impact by encouraging product sharing and promoting reuse of goods. What’s more, it supports the all-important question of affordability for bigger ticket items by spreading the cost over a series of smaller instalments, rather than the full value at once. I see new leaders emerging in the shape of platform enablers that help companies launch rental and/or resale solutions and companies directly

providing consumer PaaS solutions, such as platforms to rent or offer products like electronics via subscription. This is one of the big revolutions to come in consumerism and will only be accelerated post Covid, which has shown how fragile supply chain and international trade really are.

Opportunity 4: Extending product life

Increasing the lifespan of a product and encouraging resale and/or sharing of items through the circular economy and secondary markets extend the life of the goods and helps tackle waste. But the problem with PaaS models is that they rely on the customer to take care of a product they don’t own. When they don’t take care, it erodes residual value and slows the creation of strong secondary markets.

To get around the problem, machine learning and new technologies are being applied to make more efficient use of goods and carry out predictive maintenance before a product breaks down. Unsurprisingly then, I think we’ll see growth in refurbished and second-hand marketplaces, connecting buyers with professional sellers to acquire goods at reduced prices. Also in predictive maintenance providers, such as cloud-based software solutions that help assess residual value or reduce unplanned downtime.

So, where do we go from here?

The SuFi space is, of course, broader and more complex than what’s outlined here alone; (green) energy, commodities and sustainable housing all deserve further exploration. But SuFi is ripe with opportunities for those who can smooth the transition to net zero. By tackling the issues from two directions – through new ESG platforms and assets that improve measurement; and by helping to grow the circular economy through PaaS and product life extension – we’ll help to turn the tide on sustainability.

And the key to all of this is better data. This way, we can combat greenwashing, companies can build trust, and investors and other financial backers like Mouro Capital can continue to direct funds to those that have a true (and provable) positive impact on the environment and society. And last, but not least, better data makes it easier to predict areas where the right investment can lead to more sustainable practices in future, creating a virtuous circle of benefits for everyone.