A story where payers and those accepting payments constantly change places as both intermittently lead the evolution of payments:

Without going too deep in the backstory of payments (lest we discuss the theory of fiat money as either a exchange token or a trust medium enabling the underlying exchange of goods): the last 80 years of payments using cards was about simplifying acceptance of either money that consumers carried or allowing them to extend the personal tab from a single merchant to the whole network of a universally accepted trust mechanism.

Several years forward, acceptance of a particular method became a channel of attracting clientele of particular life choices and income band — allowing merchants to receive a larger footfall from the funnel that caught wind of ability to live on credit and rolling over the purchases over equal instalments in the future.

Where it was banks and schemes: their ability to scale their operations and command millions of users, investing in loyalty schemes (learning from casinos and airlines): merchants followed and the big breakthrough was the onset of the Web and then mobile phones.

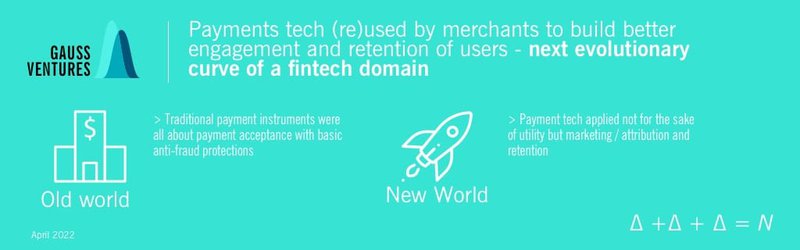

The development of personalised experience on everconnected mobile platform turned the table: the users are now led not by tokens providing means to pay — but by merchants generating user-cases — or user-stories.

Hence, its now a merchant that seeks as to how convert the user-base it has built a vast personal profile on consumers — through payment elements rebuilt around provoking next marginal purchase while securing near-instant settlement.

Where interchange regulation dampened issuing side share of the equation, acquiring return rate sat on ability to:

- Lower fraud (hence the “card-on-file” drive that still remains) while cutting “unnecessary” costly elements like 3D-Secure — equally around fraud as well as cart abandonment ratio.

- Stimulate next purchase: doing this via instrument of a plastic token rendered digital was not possible and offers after payment has been made banks do worse than a merchant

What merchants required was a payment infrastructure of their own — and fintech revolution (democratisation of both tools to build new services and capital available to fund development of these tools) enabled that.

Fast forward to today:

- Platforms built better instruments to retain users and combine elements of accepting payments with adequate loss rate (where not just fraud but cart abandonment is calculated)

- Platforms have a better retention rate stimulating transactions. Merchant-led platforms (and fintech platforms built by or in cooperation with merchants) are better tuned to react to interchange fee regulation and react to build user experience, where percentage rate / chance of additional x-sales lead to improve contribution margin on top of near-zero original transaction.

Hence presence of wallet models is not because banks are ineffective, but because banks cannot by themselves aid the closing of sales: hence merchants are building the stack themselves, or selectively participate with wallets that aid into conversion of users with means to pay into high-transactional MAU.

Merchant platforms drive further evolution of accepting payments though seeking to embedded additional information about users preferences. Not surprisingly, leaders in this are marketplaces — who convert their claimed competence of user-conversion in the fee structure for 3rd-party merchants.

Ultimately, the original promise of a cashless payment token to promote painless transactions at merchants accepting them remains — but with necessary upgrades merchants seek in them:

- Integration in customised checkout scenarios

- Carrying additional information for n+1 sale

- Providing reassurance for consumer while securing settlement for merchants / vendor

What might happen — will happen

- Card-on-file platforms and further integration / cooperation between such platforms and merchant aggregators / platforms. Enabling not just the utility of paying from consumer perspective, but promise of merchant interest to work with algorithmic B2C payment platforms like it.

- Transactional loyalty — as indelible element to compensate for IRF regulation: enabling x-sale impulses via the same protocols of accepting payment — automatic redemption will aid merchants seeking consumers and having a standard payment token — adding to the magic of both having the cake and eating it too — receiving cashback or BNPL cost coverage without additional steps.

- Merchant led adoption of payments based on open banking and open data formats: advent of BNPL models rebuild the view of traditional credit card / installment finance — putting it on new rails. Merchants already having the pull power of user-base will construct B2C payment options themselves — or through JVs, while connecting them to underlying plumbing of bank accounts.

The above three comes together as the overall ongoing transformation of ecommerce drives migration towards recurring payments, instalments, try before you buy — and all that influencing the design of payments and loyalty.