No matter how you may call it, FinTechs or TechFins, you would still be talking about ventures, new businesses and companies that should, at some point, yield some reasonable return to their investors. Over the years, I have been caught by surprise by the fact that many investment decisions were just ignoring or failing to incorporate the potential returns a given FinTech could deliver. Surprisingly or not, this continues to happen, maybe more frequently than ever.

In a world of increasing interest rates, returns should deserve greater attention. The point here is about the importance of properly assessing the returns and not about discussing the profitability levels a given company might attain in the future. In coming articles, potential returns might be the focus. Before that, we should focus on calculating accurately the profitability. For anyone mastering the four basic mathematical functions, this should be no problem.

For years, banking analysts have been working with the concept of tangible book value and return on tangible equity (ROTE). Despite the natural limitations intrinsic to any methodology, this approach helped compare the returns of different banks in different cycles. Returns on tangible equity might clearly overstate the profitability of banks that have undergone major M&A transactions once goodwill is excluded from the denominator. On a credit risk standpoint, however, it offers a more appropriate starting point to compare the financial health of different banks.

When talking about FinTechs, little is usually said about profitability. Rarely, return on equity (ROE) is highlighted in sell-side reports. While this might be partially explained by the fact that many FinTechs are startups, this should not mean that financial returns should be fully overshadowed by other KPIs (user base, TPV, ARPU, etc.). Among the many subsectors that FinTechs might be operating in, payments seem to be the one in a more mature stage of development.

Despite having a great number of companies already listed (PayPal, Square, Affirm, Stone, PagSeguro, Cielo, Getnet, Visa, Mastercard, among many others), growth potential continues to attract more attention than current and future profitability.

In Brazil, due to the accounting standards set by the Central Bank of Brazil in 2017, payment institutions (like merchant acquirers and certain digital banks) are required to recognize the receivables from card issuers and payables to merchants in their balance sheets. We are in 2021. This is not new. However, few seem to be the analysts and investors properly incorporating the existing particularities for the calculation of the profitability of these companies.

For the calculation of the ROE, no adjustment should be required. Simply dividing the reported net profit by the reported shareholders’ equity should do the magic. The net profit adjusted for stock options should be avoided, but this deserves another article. The problem, however, lays on the fact that ROE is a poor indicator for assessing the profitability of payment companies.

Combine earnings growth and ROE as the metric for management compensation and you might have the recipe for disaster. Earnings growth can be easily inflated by the prepayment of merchants’ receivables. Since merchants receive the money from sales done through credit cards in 30 days, payment companies usually offer earlier payments in exchange of a percentage fee. This can be done by simply allocating more cash into the operation.

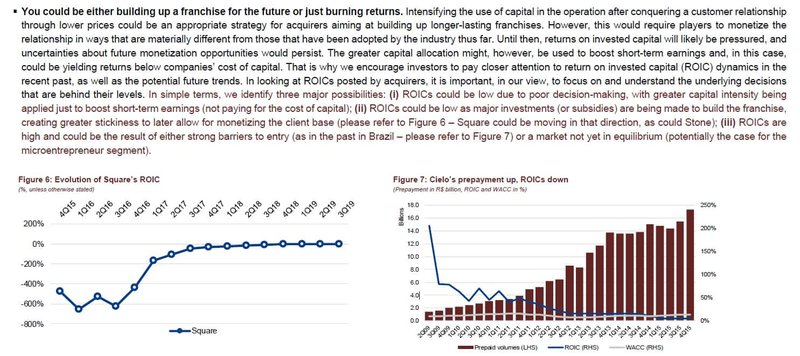

Why should this be a problem? Prepayment revenues boost earnings growth. Using own cash, however, reduces the optimization of the equity, once the likelihood of buybacks and dividends become more limited. Those bullish on payments might argue that prepayment spreads are great and, thus, the returns of the companies. Take a closer look at ROEs and the scenario becomes less glossy. High prepayment spreads are unlikely to be sustained. In certain niches, they are already gone – large merchants. In others (i.e., longtail), they might endure, but are expected to face growing competition from other means of payment. Throughout time, payment companies have been lowering the price of other services (transaction processing, rental of POS terminals) to boost prepayment revenues.

The reality becomes really frightening when third-party cash is deployed in the operation. Since many investors do not know that receivables from issuers are lowered by debt facilities structured by payment companies, the real picture of the companies’ indebtedness is usually not properly captured by the market. And this has a major implication to returns on a return on invested capital standpoint (ROIC) – the metric that more properly reflect the profitability of payment companies, in my view. Below, an extract from a report published by me on December, 2019, Payments Are Due (Bradesco BBI):

In the past, many colleagues questioned the incorporation of the money raised through these debt facilities as part of the invested capital. Why considering it as debt if the risk is very low (credit risk of card issuers) and the timeframe for receiving the money is just 30 days? My answer was always: it is a true part of the payment operation and is working capital allocated in the business. It can be either own cash or third-party cash. So, it must be considered for the calculation of the invested capital.

Now that interest rates are going up quickly, it is becoming clear to many investors that certain returns are not as high as they initially thought. In many cases, the returns (ROE or ROIC) are inferior to the cost of equity (Ke) or weighted average cost of capital (WACC). Instead of generating long-term value to shareholders, many companies might be doing the opposite. While earnings were growing, value destruction was overlooked. Once earnings surprise on the downside, value destruction becomes painfully tangible.

Why nobody cares about FinTechs' profitability? People care, but not that often.