Over the past two years there's been a rapidly growing shift in the financial services industry towards creating a continuous KYC approach, moving away from traditional periodic reviews. With regulators increasing pressure on financial institutions to enhance their KYC refresh efforts, the benefits of adopting a continuous KYC model are clear. Financial institutions can expect to gain considerable efficiencies, from reducing the time-to-revenue for new customers, to reducing operational costs and drastically improving the customer experience.

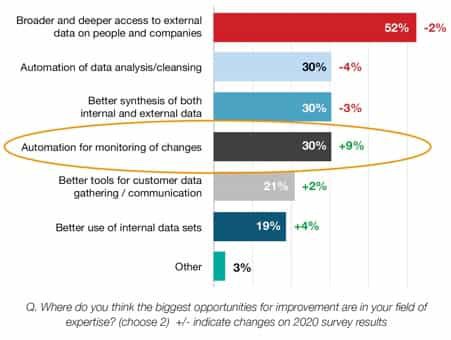

This shift was confirmed in a recent Arachnys KYC survey, where there was a marked increase in the number of industry professionals looking to automate the monitoring of customer changes.

“A point in time KYC review can be both ineffective and inefficient. The moment it is completed it is stale and can leave the door open to unnecessary risk. The only reasonable point in time review should be at onboarding, from that point on KYC should be fluid and dynamic. Automated tools that identify customer risk through continuous monitoring, while only surfacing what is new, save time and enhance the control environment.”

–Chuck Taylor, Executive VP, Head of Financial Crimes Advisory at AML RightSource

The data challenge

A recent Perpetual KYC workshop hosted by Beyond FS, also confirmed the industry demand for automating client monitoring. A poll held during the workshop indicated that 73% of the audience were engaged in planning or working towards the delivery of Perpetual KYC. In parallel, 50% of the attendees felt that the management and control of data will be the most significant barrier to implementing Perpetual KYC.

How banks achieve continuous KYC is not without its challenges, something that David Buxton, Arachnys CEO & Founder, looked to address in the workshop. One of the core challenges is around managing increased data volumes, which can be broken down into three areas:

Search – identify the most relevant data for your client population and develop automatic data resolution across multiple data sets to ensure that you are applying the most recent information.

Retrieve – apply regulatory rules to ensure that you obtain relevant documentation to support your client data and that this data is sourced from the right documents or repositories.

Consume – ensure unstructured data can be managed by converting this to structured formats to enable easy consumption into your systems.

Reducing the KYC burden

Continuous KYC looks to minimise burdens that have troubled analysts, compliance officers and system architects for some time. To achieve it, there are three pillars of data to be considered:

- Driving efficiency with self-reported customer data

- Using automation to capture and screen external data

- Reducing risk through monitoring transaction behaviour

Optimizing the processes for gathering, storing and reviewing these three pillars of data, and making them work in tandem, is the ultimate way to achieve perpetual KYC. Once achieved, financial institutions can make significant savings in costs and resources, reduce the burden of KYC and periodic review and drastically improve onboarding times, time to revenue, the quality of customer files, and the overall customer experience.

Implementing the approach

Achieving continuous KYC is a non-trivial exercise and requires a transformational approach within a financial institution. In addition to the data challenges, are the actual monitoring capabilities that are critical in the move away from the manual review of customers. Employing straight-through processing (STP) techniques are one way to replace manual processes and can vastly reduce the burden for low and medium risk customers.

It is also well accepted that the key to achieving a continuous KYC involves creating a single customer view. This can create additional challenges in terms of breaking down siloed data and synchronizing all relevant data feeds, but once obtained will dramatically improve efficiencies and increase data sharing internally.