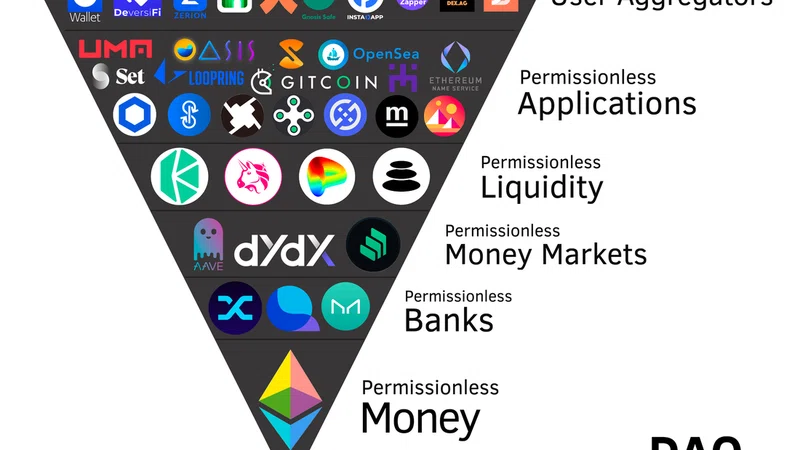

The digital banking landscape has seen a considerable change in 2021, thanks to advances in technology and a continued progression into customer preference development. Digital banking apps have been on the rise with remarkable investments into fintech unicorns such as Revolut, Nubank, and N26.

These companies are at the forefront of the development of Superapps, or financial apps or browsers that provide various financial services via a single mobile interface. These apps solve one of the biggest challenges in fintech, which is creating an integrated financial ecosystem with all the functions necessary to offer a complete experience. This also means creating a product that competes with the rest of the financial applications located on a user's phone. Becoming the only app consumers rely on for all their financial services allows the company to gain total control over multiple individual markets and earn various income streams from one consumer.

The critical ingredient for the formula to work is to develop an app that users want to return to again and again organically. This requires satisfying all of a customer's financial needs, offering such an extensive range of operations that it becomes uniquely relevant to its competitors in its variety of functionalities. This gives the Super App a competitive advantage that has catapulted the most recent complete apps, like Revolut, to the top of the market.

It offers true convenience to the consumers by allowing them to complete a series of daily financial tasks without needing to switch applications, becoming an everyday part of the customer's daily habit.

Superapps typically offer a range of the following connected financial services, among many others:

- Banking, payments, and other financial services, such as loans, savings, investment, trading, cryptocurrencies, sending and requesting money.

- Financial products beyond banking, such as insurance products for home, auto, health, and ID theft.

- Lifestyle and travel benefits, like concierge service, lounge access, ticket booking, hotel and restaurant booking, and loyalty programs.

- Government and administrative services, such as ID, registrations, taxes, paying fines, etc.

The Neobank and Traditional Bank Problem

This is providing problems to neobanks and traditional banks. In the past, these two sects of fintech have been at war competing for market share amongst themselves, but with the emergence of Superapps, they are forced to come together to combat the growing market share Superapps are grabbing in the industry. Superapps are beginning to blur the lines between a consumer’s social life, retail life, and financial services life, giving companies increasingly large holds on valuable data they generate. This data, generated from a broad range of functions, gives treasured information and insight into consumer behaviors and provides possible changes to products and services to target these customers better. With the dependence on Superapps increasing, more data is being generated, allowing Superapps to better understand their demographic and predict buying patterns and behaviors while providing the consumer with smoother, more personalized services and products. Meanwhile, neobanks and traditional banks are losing customer data and the customer market share, leading to less data to make informed consumer decisions on services and products, resulting in failed consumer expectations.