Traditional banks (especially retail banks) are facing a huge invasion of fintech. Armed with exceptional technologies and a large amount of data, fintech firms are continuously threatening the realm of existing banks. The rapid growth of Kakao Bank, a major Korean internet bank, is a good example of this movement. The number of customers of Kakao Bank surpassed 10 million within two years of its launch. Considering the population of Korea is around 50 million, this is a remarkable achievement.

As a person working for a ‘traditional’ bank (especially retail banking part!), I believe traditional banks already have a certain answer to overcome this situation — Banking-as-a-Service (BaaS). Now, I’d like to share the reasons why I believe BaaS should be and can be our answer to fintech. Before, I’d like to start introducing BaaS briefly.

BaaS is a solution that connects banks with their clients and enables clients to provide banking-related services to their own customers. It utilizes banks’ APIs banking licenses and other assets for that. Please refer this article from McKinsey for more information; https://www.mckinsey.com/industries/financial-services/our-insights/banking-matters/what-the-embedded-finance-and-banking-as-a-service-trends-mean-for-financial-services

Although it needs additional investments in technology and infrastructures, BaaS is still an attractive tool for banks, and here are the reasons:

Connecting Legacy and Future

With the rise of smartphones, customers are becoming more dependent on mobile services. Now, customers are shopping and paying with their cell phones. The pandemic accelerated this change, and fintech is creating disruptive innovation. Therefore, more and more businesses are coming to the mobile platform area, and they’re eager to integrate banking services, such as payments, into their services to advance them. However, the integration process is not a simple and easy one.

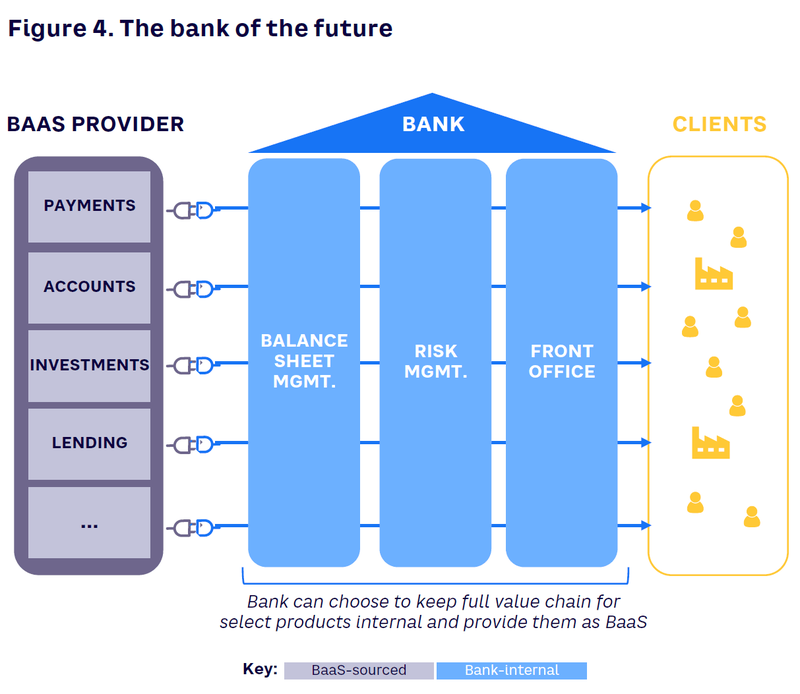

The builder should prepare all infrastructures to build a banking system — from basic account management systems to risk management systems. Moreover, the builder may need to acquire a banking license. By connecting potential partners with banks and their systems, BaaS enables them to utilize banking businesses and build advanced services based on them. For banks, BaaS helps them expand their business further without direct competition. Moreover, banks are able to lead the disruptive digitalization process. In short, BaaS connects the legacy and expertise of the traditional banks with innovative companies with a fresh idea.

Versatile Solution for Every Client

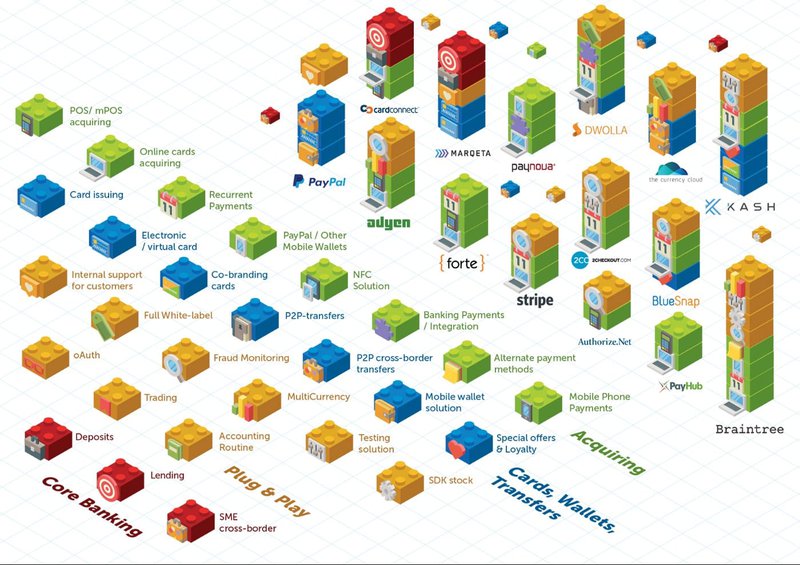

Bank-as-a-Service.com organized types of fintech APIs like the following:

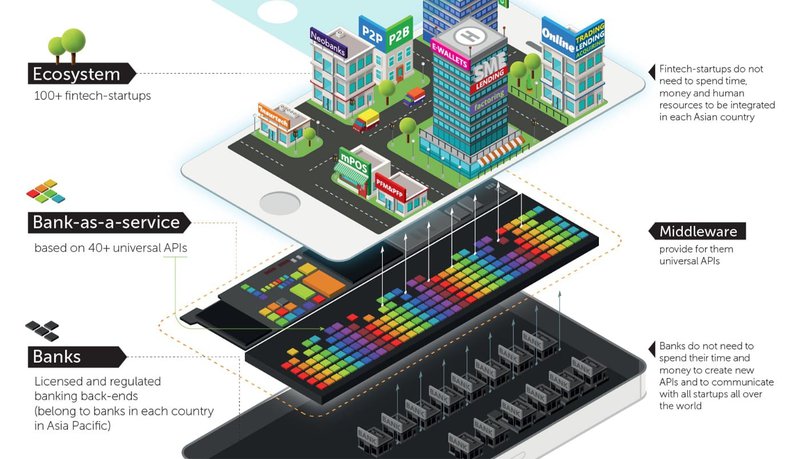

As the picture above demonstrates, an endless number of partnerships or integrations can be generated; BaaS is a hyper-versatile solution for every customer. BaaS providers, especially banks, can tailor their solutions for individual partners, and partners can advance their UX based on the individualized BaaS solution. Moreover, BaaS providers and partners can build a comprehensive ecosystem like the following picture:

Also, not like other ecosystems, there are no entry barriers against new or potential participants. The lack of entry barriers promotes the diversity of BaaS partnerships, leading to the next part.

Inclusive, without Any Barriers

Currently, to join any kind of ecosystem, new participants have to ‘join’ the ecosystem by adopting the ecosystem’s policies (e.g., developers should follow Apple’s policy and tech to participate). This system enables a strong unity but creates a high entry barrier. In contrast, BaaS does not require partners to follow providers’ policies.

Banks offer tailored solutions to their partners through BaaS solutions. The tailored services allow banks to attract partners outside of the banking business while respecting their characteristics. This way not only enables the bank to build a comprehensive ecosystem but also accelerates the diversification of the ecosystem. Various types of partnerships show this tendency well. BaaS is being used in multiple industries; from investment (Bancorp & SoFi) to e-commerce (Standard Chartered & Bukalapak, and expected to expand further.

I firmly believe that BaaS will become the future of banking, and keep studying BaaS. Recently, I’m participating in our bank’s Intrapreneurship program with my idea based on BaaS. It’s a small start, but I believe I can generate more value in BaaS and look forward to pioneering my future in BaaS.

These are great articles and reports about BaaS:

Overview of APIs and Bank-as-a-Service in Fintech, Bank-as-a-Service.com https://www.bank-as-a-service.com/BaaS.pdf

Banking as a Service, Explained, Deloitte Digital https://www.deloittedigital.com/content/dam/deloittedigital/us/documents/blog/offering-20210727-blog-baas.pdf

The Rise fo Banking As A Service, Oliver Wyman, https://www.oliverwyman.com/our-expertise/insights/2021/mar/the-rise-of-banking-as-a-service.html

Banking As A Service, Arthur D. Little, https://www.adlittle.com/en/insights/viewpoints/banking-service