Do you know how Revolut manages to scale internationally so rapidly while expanding their product portfolio? The answer lies in white-labelling APIs of multiple “Financial Infrastructure as-a-Service” (or FIS) players below. Revolut, similar to Chime and many others, is a consumer interface stitched together on the back of these infrastructure players.

Revolut is made of following components:

- DriveWealth powers commission-free trading

- Truelayer unlocks funding instruments

- Data API enabling customers to connect their external bank accounts to Revolut in a few clicks

- Payments API to enable customers to top up and access funds instantly, in real- time, without having to enter card details or share their bank credentials

- Simplesurance: cell phone insurance made simple

- Lending works: Make borrowing simple for Revolut users by delivering instant Credit

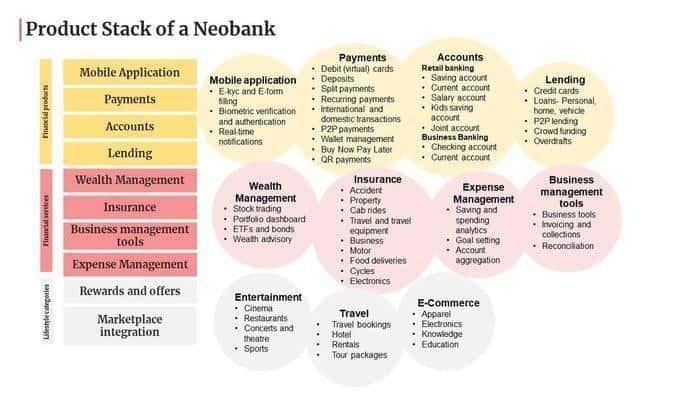

Each layer of the Product stack of neobank is increasingly being served by third-party providers who specialize in the layer (or aggregators)

Revolut is not unique here.

- Chime and Varo are basically built on top of all of Galileo’s products

- Robinhood, Monzo, Transferwise rely heavily on Galileo for various products (card issuing, auth, balance management, early deposit access)

- Cash App relies on Marqeta for cards and DriveWealth for fractional trading

- Credit Karma, Betterment, Moneylion use Cambr for cash management suite and high yield saving accounts

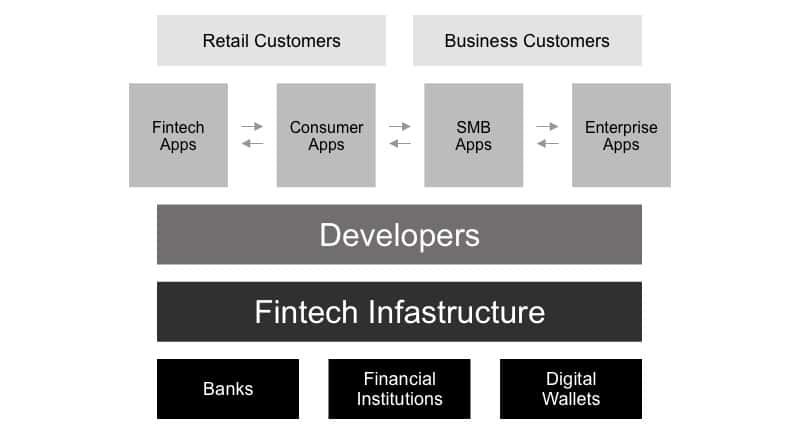

What is Financial Infrastructure as-a-Service ?

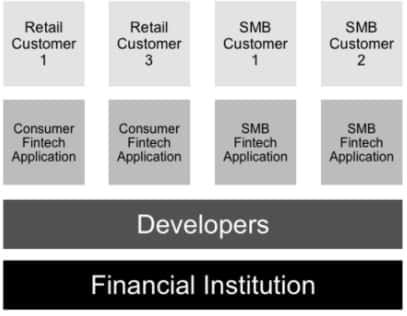

Financial Institutions were built to onboard retail consumers or SMBs and not developers. However, today there is a new class of users needing access to the underlying financial infrastructure these banks use - developers.

To serve retail and SMB customers with products such as banking, credit, trading and KYC, it took multiple years to get up and running via tech partnership, and even longer if built in house. FinTechs/Developers had to repeat cycle as product suite expands to include new products and services. With new FIS providers, the benefits are apparent around significantly faster GTM versus in-house build, ability to re-use the licenses and regulatory compliance and ease of adding new products and services to their product suite.

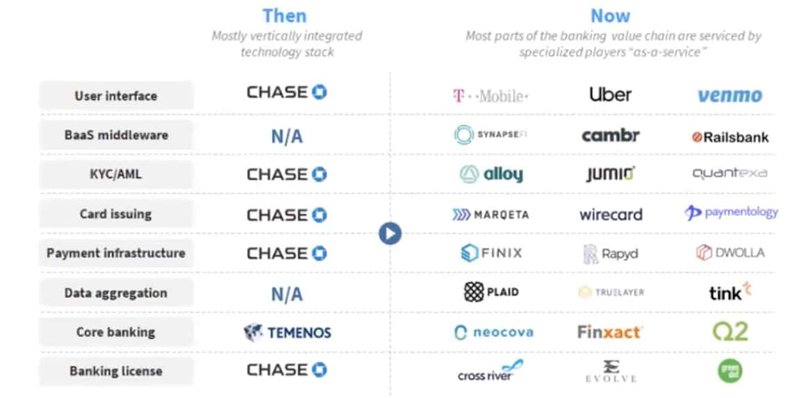

The evolution of financial services

Phase 1 “Universal Banking”:

Traditional banks cross-sell a broad suite of services to their entrenched customer base (think Chase, Wells Fargo etc.)

Phase 2 Unbundling of banks:

Gradual emergence of vertically focused financial services which have friendly APIs focused plays but still limited (e.g. QuickenLoans for Mortgages & Loans, PayPal for Payments)

Phase 3 Re-bundling of financial services:

Developer-first fintech platforms building fintech apps on top of the legacy and next-generation financial infrastructure. (Allows Chime and Revolut offering multiple value props in financial services on the back of players such as Galileo)

Key factors driving adoption of FIS players

- White-label payments infrastructure automates payment/infra operations, reducing headcount for Fintechs. It allows them to expand their product portfolio, improving stickiness and better monetize users

- Fees are often lower than with FIS players

- Access to richer consumer data which can unlock other use cases in the business (e.g. fraud products on Plaid). Fintechs can also gain control over the customer support experience — most importantly, the ability to deal with the sensitive issue of chargebacks and remediation

- Global trend towards open banking led by PSD2 in Europe and UPI in India

- Expediting time to market with developer friendly APIs, usage based pricing and SDK integration

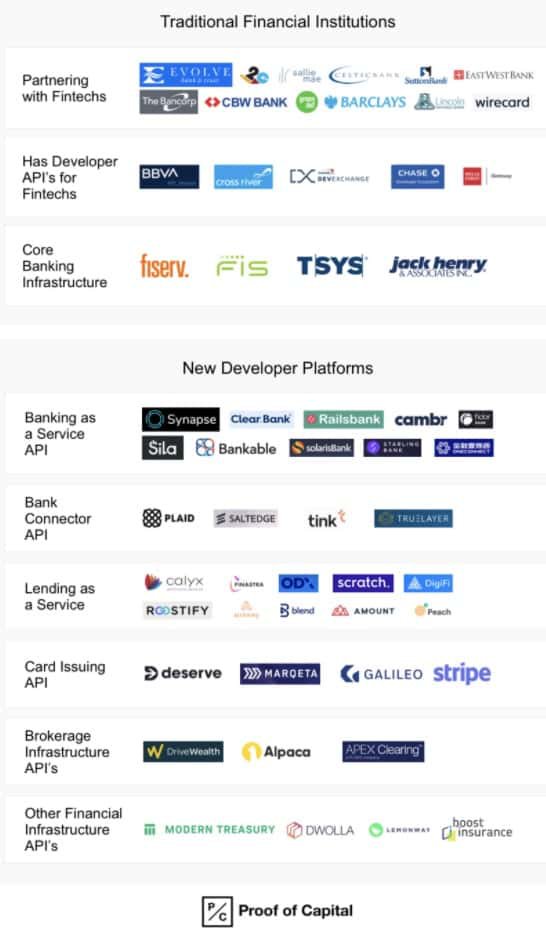

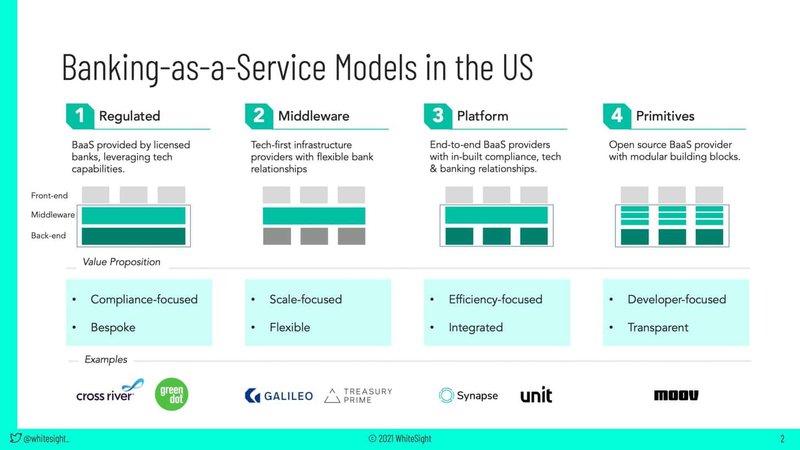

Industry Landscape of FIS players

Financial-infra-as-a-Service (FIS) is a key piece of the US fintech puzzle due to the lack of a regulatory framework for fintech specific licenses. It also has the conventional upsides that come with the service offering - doing away with cumbersome licensing requirements, faster time to market & product development, ability to focus on customer servicing and so on.

Over the years, the most populated fintech ecosystem of the world has seen numerous FIS providers coming into the picture, and they can be broadly categorized as follows:

🏦 Regulated Banks like Cross River, Green Dot Corporation utilise their licenses as well as modern tech stack to help fintech startups build on top of them.

⚙️ Middleware providers like Galileo Financial Technologies & Treasury Prime facilitate the tech infrastructure that can act as a flexible intermediary to foster collaboration between banks and fintechs.

🔌 Platform BaaS providers like Synapse & Unit provide an end-to-end offering that is ready to use for fintech startups.

🏗 Primitives, a newly emerging BaaS model, like Moov Financial offer granular control to developers designing financial products from the ground up.

Source: WhiteSight

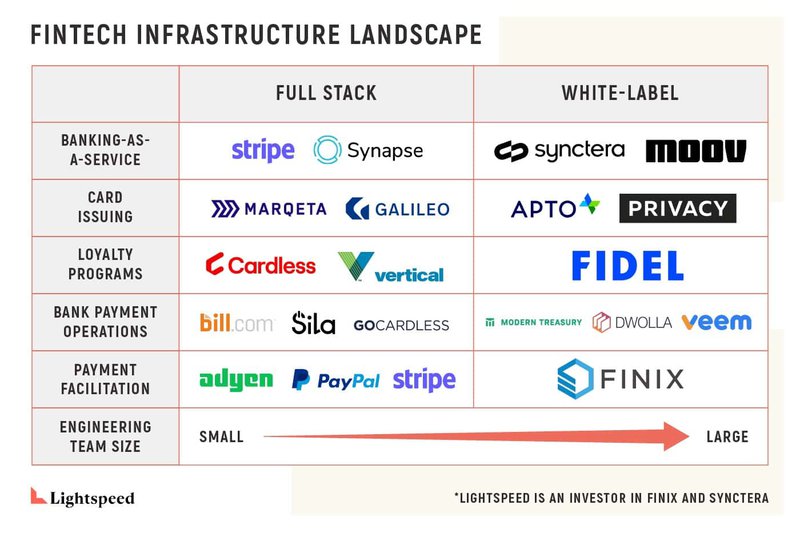

The landscape of API-as-a-service providers to the FinTech ecosystem is quickly expanding as both startups and incumbents look to scale product offerings without building in-house:

- Bank connectors and data aggregators APIs: Platforms that connect to bank and financial accounts to aggregate information + often have read/write capabilities. FinTech companies and existing financial institutions utilize APIs of Plaid, Yodlee, MX etc. to enrich customer information and often offer personal financial management tools to users

- Banking-as-a-Service APIs: Provide the entire functionality of a bank (Deposit, Savings, Send, Withdraw) to developers to allow them to build financial features within their own applications.These often connect to ‘sponsor’ banks to enable fintech companies to operate under banking regulatory environment, often providing the benefit of underlying licenses

- Payments & Card APIs: Platforms that enable FinTech companies and non-financial marketplaces to facilitate payments. Solutions vary and include facilitators, gateways etc solutions that enable companies to launch and manage payments in-house. Platforms allow developers to issue cards (Credit card, virtual cards, and prepaid cards) within their applications to their end users.

- Lending as a Service APIs: This category are platforms who are proving end-to-end lending solutions which can be embedded within fintech applications or work within lenders & financial institutions. (E.g. Blend)

- Other Financial Infrastructure API’s

- Brokerage APIs (DriveWealth, Alpaca & Apex Clearing are top ones)

- Insurance (Boost)

- Warranty (Extend)

Models for Financial Infra players

Banking “middleware” models are well positioned to offer capabilities encompassing multiple use cases, enabling faster time to market and reducing integration complexity. Vertically integrated and regulated full stack providers can help their customers get to market more quickly and offer more direct control over end-user experiences.

TLDR; how do you gain conviction in a Financial Infrastructure as-a-Service player?

I. Platform/middleware vs Point solutions

Platforms and middleware with the ability to provide a “one-stop-experience” provider presents the most compelling value proposition. It enables a seamless experience, layering in best-in-class capabilities and customers can avoid the technical integration and vendor management complexity of onboarding point solutions separately

II. Full stack regulated providers Vs others re-using licenses

Regulated service providers can have an edge due to their license and vertically integrated stack, which offers more control over the end user experience

III. Developer first model and friendly APIs

Providers with developer first offerings such as fast onboarding, easy to use APIs, sandbox environments and rapid testing, can stand out among fintechs by proving to move faster than their in-house tech teams. These also need to be balanced against regulatory KYC, AML requirements

IV. Pricing models that don’t sting as you scale

Providers have 3 types of models: Revenue share (zero cost model), pure txn based pricing and txn based pricing per product with minimum revenues. Negotiating longer term-contracts with volume based discounts and building in flexibility for multi-tenancy can prove to be invaluable as fintech companies scale

V. Use case complexity

Among BaaS providers, there is a spectrum of products -- some are built off-theshelf and others offer a lot of customization. Companies that want to launch a banking product may require a complex use case which would require deeper access to banking and payment APIs. Others require less in-depth control of components. Based on the complexity of the use case, different solutions will be more or less appropriate

Case Study: Why I am betting on Synctera

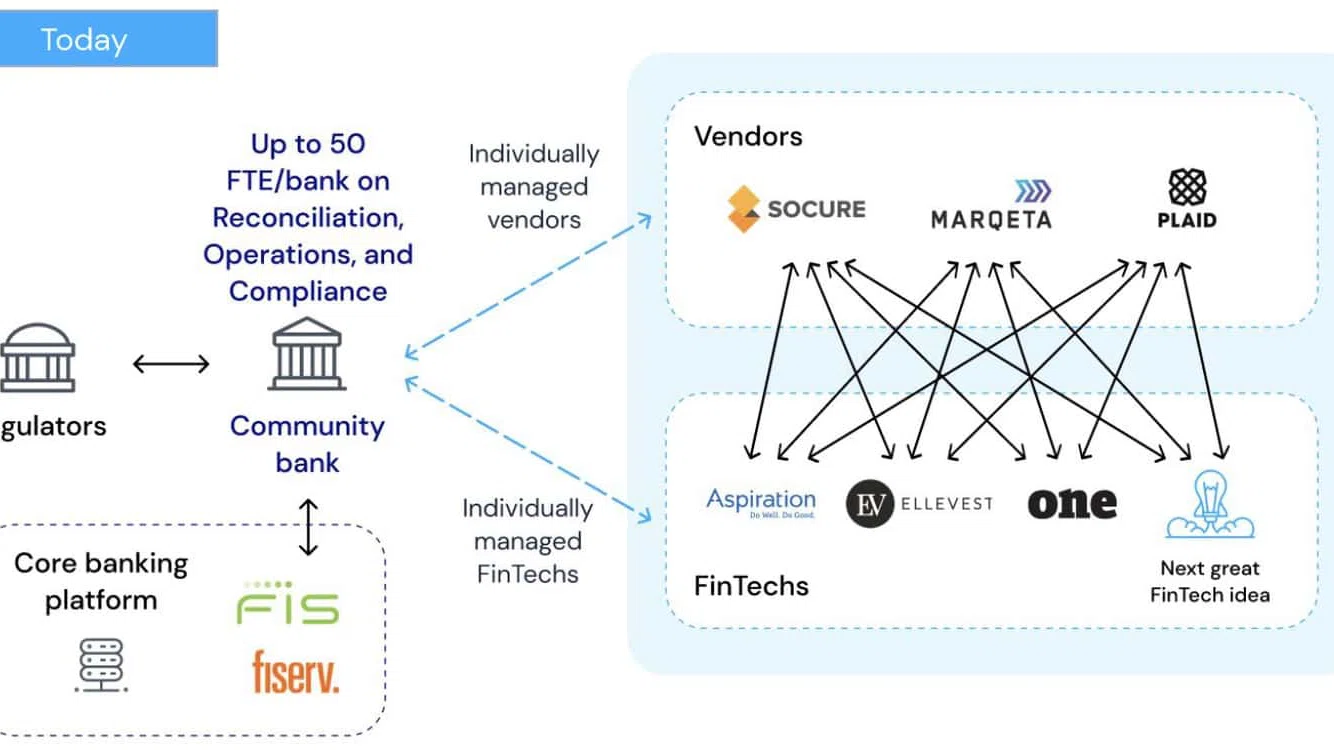

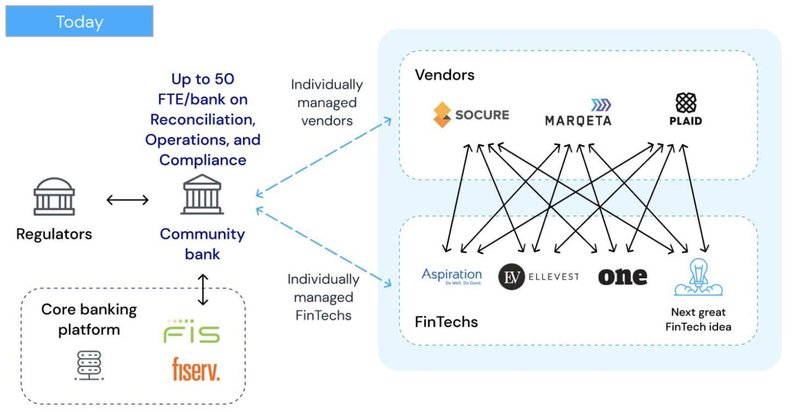

There are 10K+ small / community banks in the US which have been left behind with rise of fintech economy. However, they are now looking to actively act as Sponsor banks and partner with fintechs enabled by Durbin regulation to capture high interchange fees. BaaS channel presents a clear growth opportunity as there is no risk of cannibalizing their own banking business). It is also a natural way to compete against large banks for low-cost deposits. It is a golden opportunity to generate “fee-based income” and improve ROE.

Community banks find it very hard to partner with onslaught of fintech vendors..

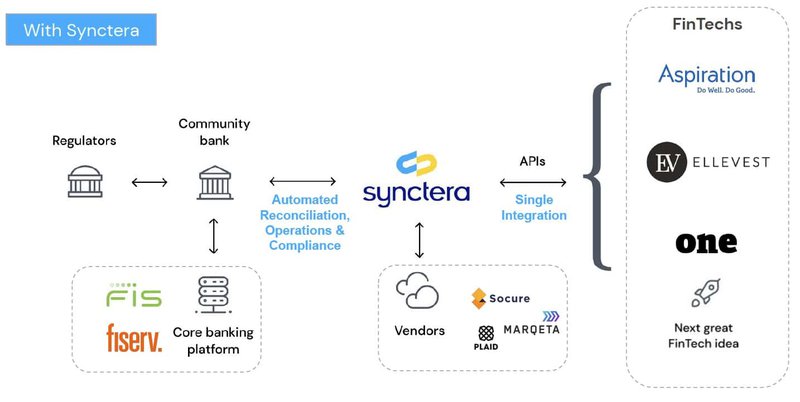

Synctera brings banks and FinTechs together and operates as a Financial Infrastructure as-a-Service

Put simply, Synctera wants to make it easier for community banks and fintechs to partner with each other. It examines banks’ needs and then sets them up with a fintech that is best suited to meet those needs. It claims to “do the work for both parties,” managing the partnership from its back-end platform, while dealing with issues like regulatory compliance, which can be a deterrent for some companies. The process of managing, reconciling and billing banks can result in “a lot of operational overhead and complexity,” according to the company.

The company says it has built a “diverse” marketplace of banks and fintech companies so that it can apply a “personalized touch to each match” and make sure that the parties “align on geography, brand ethos, and desired business goals.”

This is the reason that Synctera, which aims to serve as a matchmaker for community banks and fintechs, has raised $33 million in a Series A round of funding in June 2021

This article was first published here, you can follow the author on LinkedIn