There’s no denying it — climate tech has made a serious comeback in the world of venture. With more than $40bn deployed across more than 600 deals in 2021 and investment as a whole growing at five times the rate of the rest of the venture capital ecosystem over the past five years, interest in the space has never been higher. While funds like Blue Bear, Energy Impact Partners, Powerhouse, Congruent, Union Square Ventures, Lowercarbon Capital and many others have all raised climate tech-specific funds, generalist investors have joined the party as well, with over 1,400 firms participating in at least one climate tech deal in 2021.

As fintech investors at Anthemis, we have been particularly interested in the intersection of financial services and climate tech. From its effect on underlying risk profiles, to its impact on the energy grid, to the need for renewable energy infrastructure financing, climate change creates challenges and subsequent opportunities in the world of financial services. Part one of this piece serves to outline some of the ways in which technology can help reduce the financial risks associated with our shifting climate, while part two will focus on inherent risk mitigation. If any of the following resonates with what you’re building or investing in, please reach out — would love to chat!

New risks create the need for new underwriting models

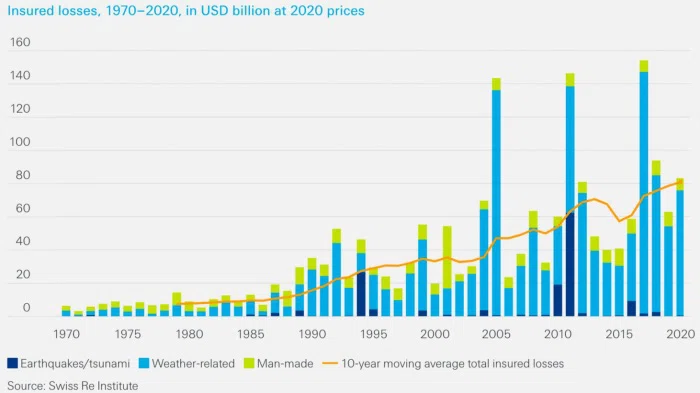

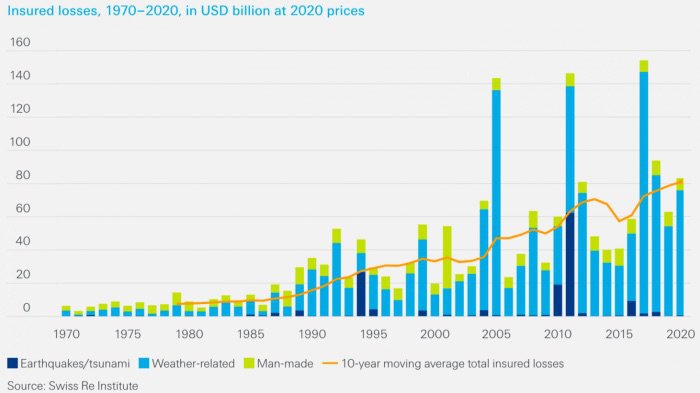

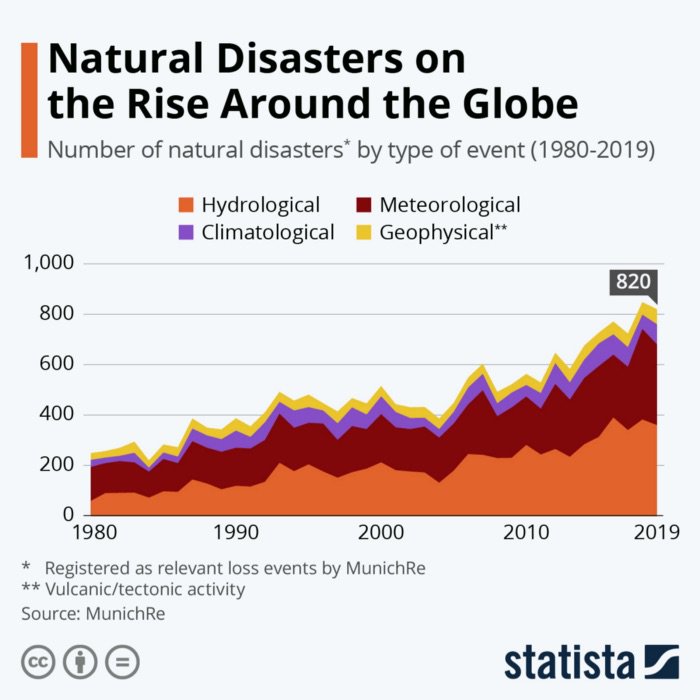

From an insurance perspective, climate change represents a major threat to the industry. As both the frequency and severity of natural disasters continues to increase, insurers’ catastrophe losses have escalated, totaling $89bn in 2020. The US alone experienced 22 extreme weather and climate-related disasters that caused an excess of $1bn in losses each in 2020.

This increase in climate-associated risk has created challenges for carriers, causing them to rethink their approach to underwriting, often leading to reductions in coverage and increased premium costs for the insured. For example, California saw residential non-renewals increase by 31% between 2018 and 2019 as a result of growing wildfire risk. Under the new “Risk Rating 2.0” system from the US Federal Emergency Management Agency (FEMA) for calculating flood rates, 77 percent of customers are set to see increases in premiums.

These complex underwriting circumstances create opportunities for startups that can more accurately price risk. At Anthemis, we’ve invested in companies like Kettle and Stable, dealing with wildfire and commodities, respectively. Others in the space include the likes of FutureProof which operates as an MGA and develops technology to effectively leverage data to gain a more comprehensive understanding of risk profiles, offering insurance products accordingly.

Parametric policies offer the potential for significant efficiency

When natural disasters occur, traditional insurance solutions tend to struggle to verify, process, and pay out claims, given the fact that the financial impact of damages must be assessed on a per-policy basis. The sheer volume of claims being processed at once leads to operational nightmares that result in real inefficiencies, with claims at times taking years to be processed. For example, two years after the disaster of Hurricane Maria in Puerto Rico, $1.6bn in insurance claims remained unresolved. This is absolutely brutal for the affected individuals and businesses, who rely on the insurance payouts to rebuild.

Climate-related risks are a logical place to start for parametric policies. The clear occurrence of a documentable and quantifiable event allows insurers to create and trigger policies in a straightforward fashion. When a natural disaster or weather-related event occurs, claims payouts are automatically triggered based on predetermined factors and preselected levels of coverage. As such, claims assessment costs for insurers can be dramatically reduced, while policyholders can see cash in days rather than potentially months to years.

Despite the obvious benefits, parametric insurance is still very much in its early days, generating roughly $500m in premiums in 2021. While the space is growing rapidly at 60% YoY, we at Anthemis believe that modern technology will be key to unlocking its potential. The execution of parametric insurance presents unique challenges in terms of policy creation and payout execution. With the former, the use and analysis of accurate data is extremely important. Since parametric policies are constructed in a forward-looking fashion (with predetermined outcomes based on the occurrence of future events), pricing must be highly accurate in order to maintain ideal loss ratios. As such, advanced predictive analytics based on a variety of granular data sources become highly necessary. Further, given that when an event does take place, a large number of policyholders will be entitled to payouts, insurers must be able to effectively manage and execute policies on a large scale.

Companies are tackling these challenges in a number of ways. Startups like Demex and Súper (Anthemis portfolio companies), Descartes, Arbol, Jumpstart, and all serve as policy underwriters, leveraging their abilities to uniquely assess and price risk. Others like Raincoat (an Anthemis portfolio company) and Plover partner with financial institutions to help create, manage, and trigger policies at scale.

Assessing climate risk requires high quality data and analytics

Increasing climate risk inevitably results in a greater overall threat to our infrastructure and physical assets.

Data aggregators and analytics providers will play a key role in accurately assessing this new risk in its various forms. In the same way that Moody’s and S&P can assess credit risk, climate risk analytics providers can pull geospatial, weather, asset-level, and other related data to create risk scoring methodologies. This intelligence can then be applied to insurance, banking, asset management, real estate, energy, manufacturing, retail, agriculture, and more in order to stay ahead of climate volatility.

Moody’s has already been acquisitive in the space, buying RMS in 2021 for $2bn. A number of startups like Jupiter Intelligence, One Concern, Cervest, Gro Intelligence, Climavision, Sust Global, Climate AI, Cloud to Street, and Terrafuse AI have all entered the space as well. While their end products may differ slightly in terms of distribution (some offering an API that provides data and risk scoring, others offering more of a dashboard to visualize risk across a full portfolio of assets), the general premise of delivering data and analytics to better understand climate risk remains.

At Anthemis, we are excited to continue backing founders who can make a real difference in mitigating the financial risks associated with our changing climate. If you’re a founder or investor in the space (or in fintech more broadly), I’d love to chat ([email protected]).