As the economic tide goes out, investors will see which of Africa’s fintech and crypto startups were swimming naked. More than half of all venture capital investment on the continent last year went to new consumer payments, banking, crypto and other services, many designed for first-time users. Products and underwriting tied to productive uses, rather than speculation and gambling, may prove the most resilient and sustainable.

The state of the market

Earlier models of financial inclusion assumed based layers of banking and finance would remain constant. However, this is not proving to be the case as new technologies are transforming the core infrastructure and delivery of a wide range of customer-facing financial products and services. The last few years have been extraordinarily frothy across all risk assets including venture capital and crypto and the bull market has given rise to fintech’s emergence as a dominant asset class in venture globally.

Fintech’s astounding growth has been a global phenomenon with fintech funding reaching a record high last year of $132 billion in 2021 (more than double the previous year of $49 billion). But in Africa, the massive funding increase is even more profound — startups raised more in 2021 alone than the preceding seven years combined, reaching a record $5.2 billion ($1.1 billion in 2020). Of this, fintech made up over 60% of capital invested — three times the global average. Crypto became a major factor in fintech funding. $127 million was raised in 2021; $91 million just last quarter — it’s still a nascent space in Africa — but it’s growing fast and there’s potential.

We attribute the acceleration of venture capital deployment in Africa to two factors. First, there is a recognition of how big a market opportunity this is. Over the past four years, markets in Africa have advanced and consumers in Africa have experienced substantial purchasing power gains. The cost of data and smartphones has come down dramatically so more people can afford to engage with digital payments, financial services and e-commerce. This rapidly expanding total addressable market is attracting the attention of high-growth, tech-enabled companies. Second, with global capital markets awash in liquidity, we saw VCs recognizing this market opportunity and stepping further out on the risk curve by pursuing emerging market investments. This includes African investors and global VC entering Africa such as Tiger Global, SoftBank, Global Founders Capital, Accel, a16z, and Sequoia.

Many capital gaps persist in African markets despite this growth. It is a fragmented market where four countries, Nigeria, Kenya, Egypt, and South Africa attracted 68% of the funding. Within the fintech sector, a small number of startups attracted an outsized portion, with four companies alone raising megarounds totaling $833 million — Chipper Cash, MFS Africa, Yoco, and OPay.

Generally, the current correction among risk assets could be seen as healthy. To quote Mohamed El-Erian, we are seeing an “unwind of the everything rally made possible by prolonged and excessive central bank market intervention.” There is turmoil across all markets and there is a lack of “safe assets” as government bonds decline and cash is pressured by the highest inflation in 40 years (of at least 8.6% for US dollars).

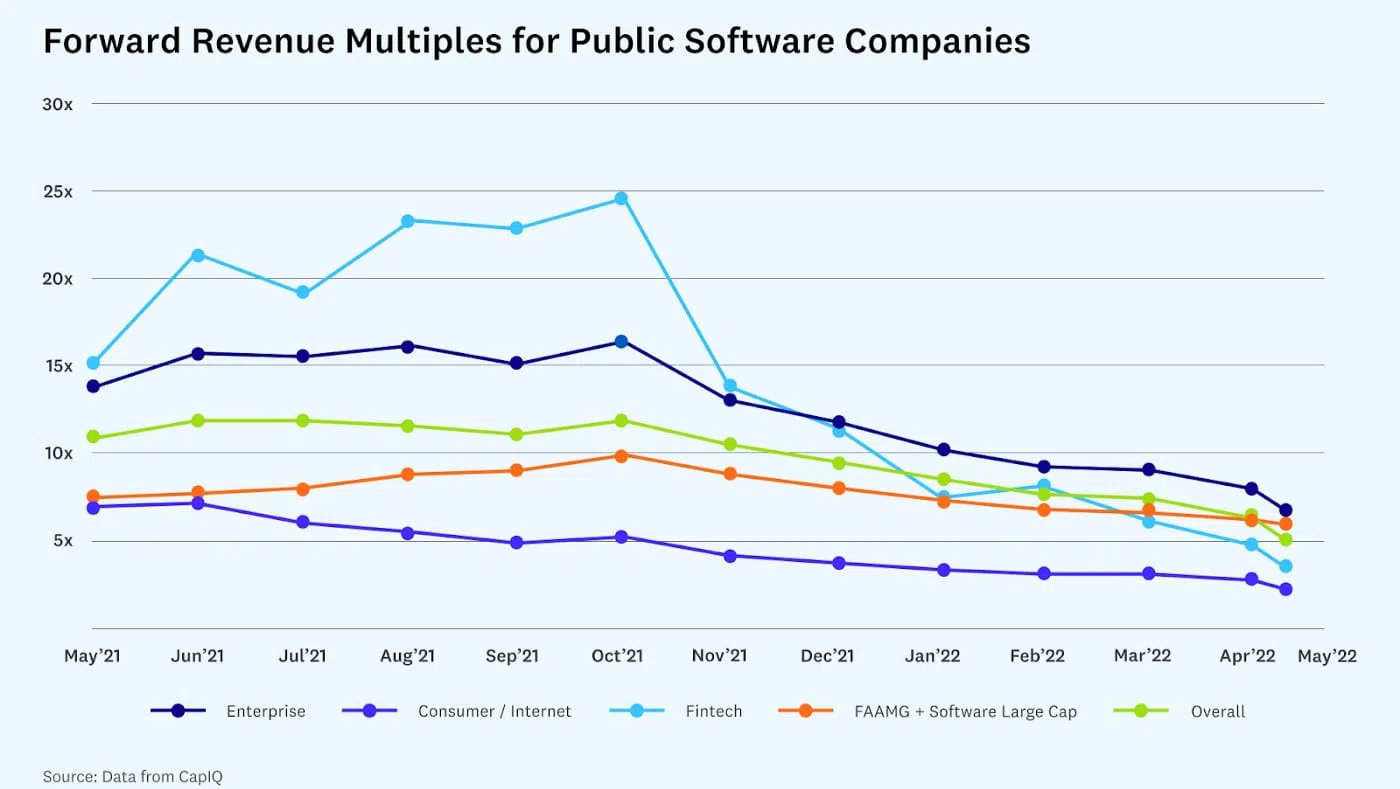

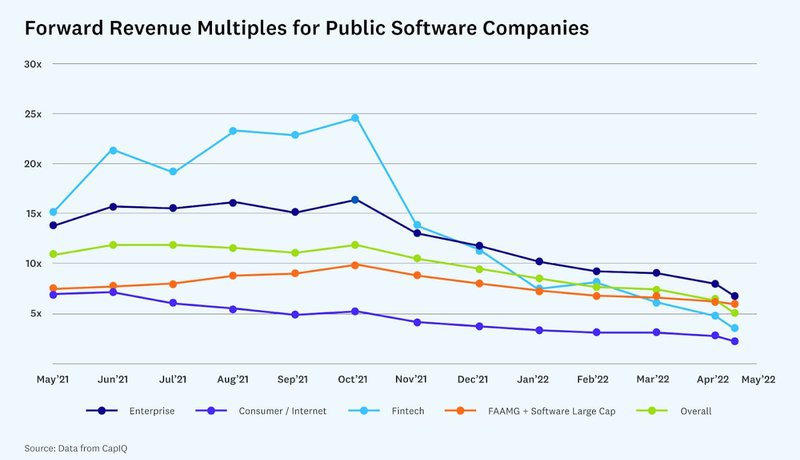

Valuations in Fintech are dropping faster than other sectors. Already, forward revenue multiples for public software companies have dropped precipitously from 25x in October 2021 to below 5x currently. We can expect that valuations of startups in Africa will follow suit and moderate over the coming months.

We are already seeing layoffs and a chorus of venture funds warning their portfolio companies to prepare for the worst. It’s unclear how deep or sustained a downturn this will be — will it be a short term correction that brings price-to-earnings ratios down closer to the mean? And venture capital valuations moderate? Or will this be the beginning of a deeper, sustained recession plagued by stagflationary headwinds? In either case, we believe it will separate the quality from the hype in fintech and crypto. The anthem of “growth at any price” is shifting and startups will need to demonstrate product-market fit earlier to raise their next round. As the market pulls back and liquidity becomes more scarce, we expect significant consolidation — unsustainable fintech startups will be outcompeted by companies with more resilient business models and more resilient users.

What won’t survive?

In an economic downturn, some of the excesses in fintech, such as the plethora of high-interest, unsecured consumer digital credit companies or get-rich-quick NFT/crypto fads, may well see user flight and credit quality deteriorate more quickly. Companies that offer products that improve the productivity and livelihoods of their customers are better placed to withstand market disruptions, while extractive and inequitable models are more likely to face the sharpest losses.

For example, in Kenya there are over 120 digital lending platforms. Some offer credit for productive uses, but many focus on unsecured consumer lending and charge APRs in the triple digits. Many are using predatory lending practices and breaching data privacy among users, creating cycles of overindebtedness. While mobile money and lending can drive financial inclusion, digital lending has also facilitated a spike in betting and other unproductive use cases by lowering barriers to entry. Instant credit or Buy Now Pay Later (BNPL) lenders that do not adequately evaluate the credit needs and uses of their customers may prove unsustainable. There has been an emergence of more “burn and churn” investing platforms — some take the guise of neobanks, others crypto exchanges — trumpeting ‘get-rich-quick’ opportunities that are selling products that don’t make their users better off. All of these business models could face substantial customer churn and struggle to survive the downturn.

What will survive?

We believe that the most resilient fintechs are those that create the most resilient users. Companies that help their users achieve true productivity and livelihood gains from digital financial services will see their customers become more resilient to shocks in their own lives and businesses. Over time, these companies will have more loyal, sticky customers with greater purchasing power which can drive better unit economics and revenue growth.

Without the tailwinds of the last few years, founders will need to reach product-market fit sooner to be able to raise funding rounds. Companies with a deep focus on customer feedback, user experience, distribution and product design are more likely to achieve this.

We back fintech startups that are driving real, measurable financial resilience, and place their users’ wellbeing at the center, through:

1) Getting distribution right with a strong ground game at the last-mile

2) Integrating customer education intuitively into the user experience

3) Product bundling and embedded finance linked to productive use.

We believe these pillars are essential to create higher levels of resilience among underserved users, as well as creating more resilient companies, themselves. Creating a more resilient user base leads to a more resilient company.

To outline some key examples, the following companies are taking a user-centered approach to developing innovative distribution approaches, bundling information and financial services, and embedding credit for productive uses:

- WASOKO

Wasoko is an example of a portfolio company focused on embedded finance, distribution and designing solutions for multiple pain points their merchants face by providing easy ordering and delivery of inventory. Embedded finance enables their informal retailers to stock more inventory, sell more, and optimize cash flow. - PIVO

Pivo is a neobank focused on providing credit for productive uses that is tailored to logistics and supply chain SMEs. This is a large and unattended market that has significant working capital requirements given the inefficiencies and time lags in global supply chains (e..g, importers, exporters, freight-forwarding, clearing agents, long haul trip fulfillment, etc.). SMEs in this sector often lack the formality or collateral to access credit so Pivo fills this gap with working capital loans collateralized by contracts from the SMEs clients (AR Financing/Factoring). Pivo’s model allows their base of SMEs, the majority of whom are women-led (in a male-dominated sector), to fulfill more orders than they would without rapid and accessible financing, thereby growing their incomes. - KUUNDA

Kuunda is another example of an embedded credit model that structures loans to drive economic gains and optimize distribution. Kuunda provides mobile money agents access to short term loans that allow them to increase productivity. Their flagship product is an agent overdraft for mobile money agents that gives them point-of-sale loans when they run out of float so they can continue serving customers with top-ups, utility bills, remittances, and a range of other products without shutting down. Loans are ethically priced so everyone wins: the consumer can perform essential transactions, and the agent/agent network makes more money from every transaction than the interest paid on the loan to Kuunda.

Another areas is customer education focused on responsible use. Companies that bundle educational resources with financial products and layer them into the user experience can build awareness and trust among their users. It can be a customer acquisition strategy that also increases retention and lifetime value of their customers:

- EJARA

Ejara promotes responsible investing with new asset classes that integrate education throughout their customers’ journey. New savings products and investment assets require education about risks and responsible use and Ejara trains their users on how to enter crypto, offers secure savings products, stable investment opportunities, limitations on volatile assets, and conducts financial training through online and offline engagements with users. - PULA

Insurance is a complex product, but can be a lifeline for more resilient farming communities affected by climate change. By bundling insurance with agricultural inputs and other financial products, and engaging with distribution and channel partners to raise awareness, Pula is proving that index insurance can go beyond protection and unlock growth potential for users. - UMOJA LABS

Umoja Labs brings transparency to last mile payments in Africa by supporting everything from USSD wallets and mass-payout tools to crypto-to-fiat on- and off-ramps focused on emerging markets. It seeks to connect 1.35 billion mobile money users who transact over $1 trillion in value to the $250B+ DeFi market. Its blockchain-based payments suite is designed to empower people across frontier markets to gain access to digital financial services.

At Mercy Corps Ventures, we’re focused on solutions that strengthen the financial resilience and climate resilience of people and communities, and are continuing to look for solutions that can provide financial services to the 1.7 billion people globally who are unbanked — 1 billion of which are women. As a pioneer impact fund investing in crypto and Web3, we know the down market will separate the quality from the hype in tech and crypto, and continue to see huge potential to democratize everything from payments, to savings, lending, supply chain traceability, insurance, land tenure, on-chain carbon credits, by leveraging decentralized technology.

For more, watch our Agents of Impact panel with ImpactAlpha.

this article was first published here