When it comes to FinTech consumer-facing business models often capture most of the attention. This article argues that small businesses in developing countries present a massively underserved opportunity for FinTech players in the post-COVID world. Small businesses in developing countries are often in the informal sector and lack access to formal financial services. Financial products offered by the traditional players to the small businesses are often either watered-down versions of products for large corporates or consumer products with some business features retrofitted to them. Lack of data brings another challenge for small businesses to avail formal financial services. The lack of focus by the traditional financial services players leaves a significant opportunity for FinTech players.

But, How big is the opportunity?

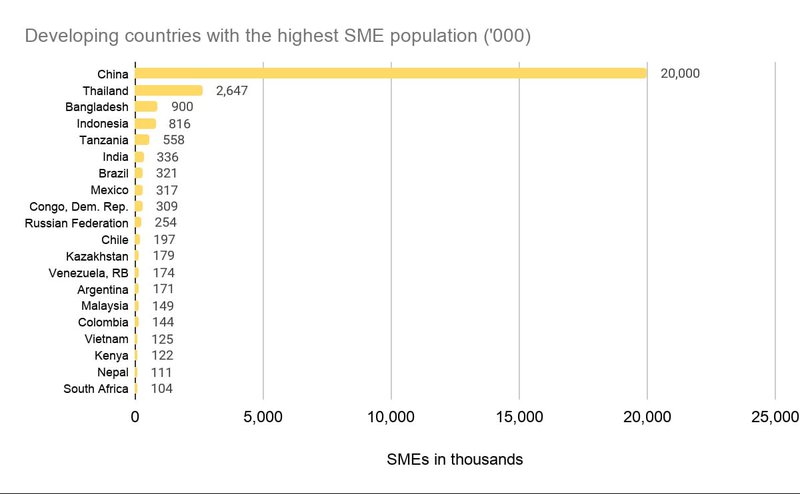

As per World Bank data, there are around 315 million Micro, Small, and Medium-Sized Enterprises (MSMEs) in the developing countries. About 90% of them are Micro Enterprises (total assets or annual sales less than US$100,000). 10% or a little more than 31 million falls in the SME category. 74 million or more than 23% of MSMEs in developing countries are located in China, followed by India, Indonesia, Nigeria, and Brazil. China is also the home of the largest SME population - 20 million or two-thirds of all SMEs in developing countries. China is followed by Thailand, Bangladesh, and Indonesia, etc. (World Bank Group Finances).

Data Source: (World Bank Group Finances)

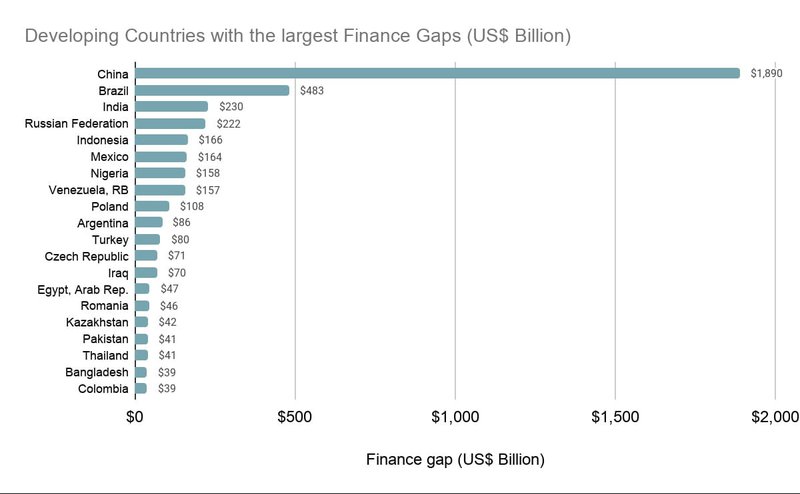

These small businesses in the developing countries deal with more than US$4.8 trillion of finance gap. China represents around 40% of that finance gap, followed by Brazil and India.

Data Source: (World Bank Group Finances)

The fragmented nature of small businesses in the developing countries along with lower profit potential per customer makes the SME segment unattractive for traditional financial service providers. But many startups are capturing this segment with the use of technology which lowers their costs both for growth and operations.

Primer on SME FinTech

Formal banking is often too expensive and involves too complicated paperwork than small businesses can afford. At the same time, banking is unavoidable to do business. Some FinTech startups such as N26 in Germany, BREX in the USA, and Atom Bank in the UK are on the mission to alleviate the banking challenges of small businesses.

Small businesses often lack well-defined operating processes resulting in productivity losses and regulatory complications. Startups such as Avidxchange in the USA and Khatabook in India are simplifying the accounting, invoicing, and tax filing processes for small businesses.

Payment is another pain point for small businesses. Startups such as Klarna from Sweden, Stripe in the USA, Pine Labs in India, and PingPong in China are providing payment solutions to small businesses.

Few other use cases of SME FinTech are Expense Management(E.g. Divvy and Swile), Procurement (E.g. Tradeshift and Ivalua), Payroll (E.g. Zenefits and Gusto), Business Insurance (E.g. NEXT Insurance and Superscript), Equity Fundraising (E.g. CircleUp and SeedInvest), and Debt Fundraising (E.g. Kabbage and Linklogis), etc.

Challenges with the SME sector

Capturing the SME segment is not devoid of challenges.

The first and foremost reason that fails to excite traditional financial service firms about the SME sector is the relatively low return on equity (ROE), about 7 to 8% for traditional financial service players (McKinsey & Company). The customer acquisition and operating costs of the traditional financial service players are often too high compared to their ability to generate revenue from the SME customers.

The second challenge that traditional financial service players face serving the SME sector is the lack of understanding of the needs of the SME customers. An investigation by the Competition and Markets Authority of the UK found that services provided by big banks often fail to satisfy the needs of small business customers (Competition and Markets Authority, UK).

The third challenge that the traditional financial services players face serving the SME sector is the lack of defined processes and lack of dedicated resources catering to those processes in the case of the small businesses. This means that in the case of small businesses banks are not interacting with finance experts but rather with the proprietors themselves who may not be trained in finance or accounting. This brings new challenges in customer service and the design of user interfaces.

SMEs in developing countries multiply the challenges for financial service providers with low levels of digital adoption, complicated licensing and regulatory structure, higher use of cash, and lack of formal processes, etc.

How COVID-19 pandemic is changing the SME landscape?

The global economy is going through some unprecedented shocks due to the pandemic. As per the International Monetary Fund (IMF), the global economy is expected to contract by 4.4% in 2020 (International Monetary Fund).

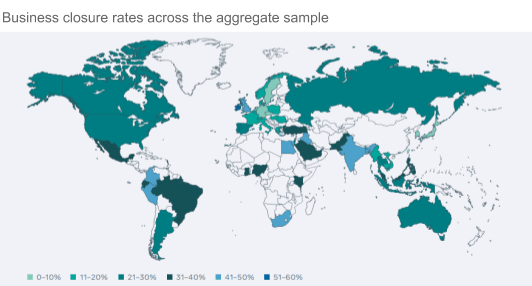

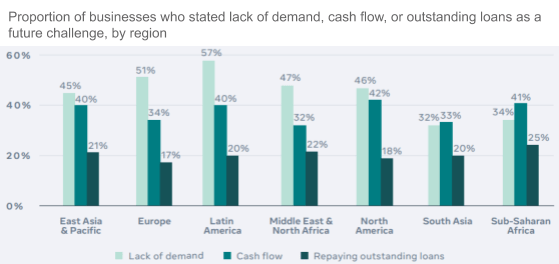

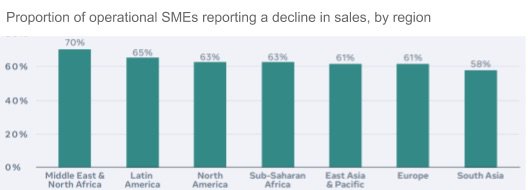

As per Facebook’s Global State of Small Business Report, 26% of surveyed small businesses closed operations during the period January-May 2020. 62% of SMEs who were operational during the period reported a lower revenue compared to the previous year. 57% experienced a sales decline of 50% or more. The most affected sectors were Hotels, cafes & restaurants, Transportation & logistics followed by Manufacturing and Retail (Facebook et al.).

Source: (Facebook et al.)

Source: (Facebook et al.)

Source: (Facebook et al.)

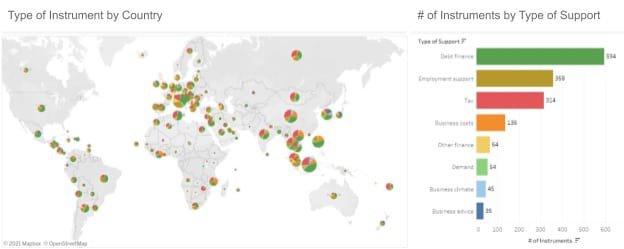

Governments around the world introduced several policy steps to protect small businesses. The steps involved debt support, employment support, tax support, steps to reduce the busness cost for small businesses, and regulatory relaxations (The World Bank).

Some governments such as China pushed SMEs for digital adoption. China introduced vouchers for remote business services and encouraged platform businesses to reduce entry costs (The World Bank).

Source: (The World Bank)

Another important progress during COVID-19 is the rapid digital adoption among consumers. A survey by the United Nations Conference on Trade and Development in China, Turkey, Republic of Korea, Brazil, Italy, South Africa, Russian Federation, Germany, and Switzerland finds that not only consumers adopted digital behaviors during the lockdowns but they are expected to continue those behaviors after we move to normalcy (UNCTAD et al.).

SMEs in the developing countries also adopted digital channels during the pandemic partly due to policy push and partly for survival. For example, As per CRISIL in India, “About 29% of the MSEs surveyed were using digital sales channels such as online aggregators/ market places, social media, and mobile marketing before the pandemic struck. That number has shot up to 53% among small enterprises and 47% among micro-enterprises as of November. Despite their limitations, micro-enterprises are not very far from small enterprises in digital adoption. Also, many more are now saying they will take the digital route soon. This underscores the fact that increasing digitalization enlarges the footprint of MSEs, helping them tap newer markets and improving their access to credit.” (CRISIL).

COVID-19 pandemic brought unprecedented devastation in the lives of billions in one way or another. The SMEs in the developing countries were not exempted. Many were forced to close their businesses, many were forced to lay off employees, and many were forced to curtail operations. As the lockdowns recede and economies open up, the SMEs need funds, customers, and human resources to start over. But, the pandemic has changed the landscape. Both the SMEs and their customers adopted digital behaviors. This creates an ideal opportunity for FinTechs who serve SMEs in developing countries. Consider Drip Capital, a Palo Alto based FinTech startup providing trade finance to SMEs in the emerging markets. Drip Capital recently crossed the milestone of US$1 billion in trade financing for small businesses (Financial Express). The company has recorded a 50% quarter-on-quarter growth in the last three quarters.

In conclusion, the SMEs in developing countries bring a lucrative opportunity for FinTech companies. The pandemic has assuaged the growth challenges for FinTechs in developing countries with increasing digital adoption and policy support. The time is now.

Cover image and charts from: Facebook/OECD/World Bank (2020), The Future of Business Survey, available at: dataforgood.fb.com/global-state-of-smb.

Bibliography

- Competition and Markets Authority, UK. “Retail banking market investigation.” 2016, pp. 308-312.

- CRISIL. “Smaller enterprises in big digital shift to shore up sales in pandemic times.” www.crisil.com, 24 December 2020

- Facebook, et al. “Global State of Small Business Report.” The Future of Business Survey, July 2020

- International Monetary Fund. “World Economic Outlook, October 2020: A Long and Difficult Ascent.” www.imf.org, October 2020,

- McKinsey & Company. “Beyond banking: How banks can use ecosystems to win in the SME market.” Global Banking Practice, 2019, p. 2. www.mckinsey.com,

- Financial Express. “Y Combinator-backed Drip Capital crosses $1 billion milestone in trade financing for small businesses.” Sandeep Soni, 14 January 2021

- UNCTAD, and NetComm Suisse eCommerce Association. “COVID-19 and E-Commerce.” unctad.org, October 2020,

- The World Bank. “Map of SME-Support Measures in Response to COVID-19.” www.worldbank.org, April 2020

- World Bank Group Finances. “MSME Finance Gap.” finances.worldbank.org, World Bank Group, 3 February 2020