Liquidity deficiency seems to be at the core of the 70% in deferred payments.

Following a recent report by the Observatory of Delinquency of the Spanish Confederation of Small and Medium Enterprises (CEPYME), during Q1 (2021) a 70% payment delinquency was recorded across diverse sectors.

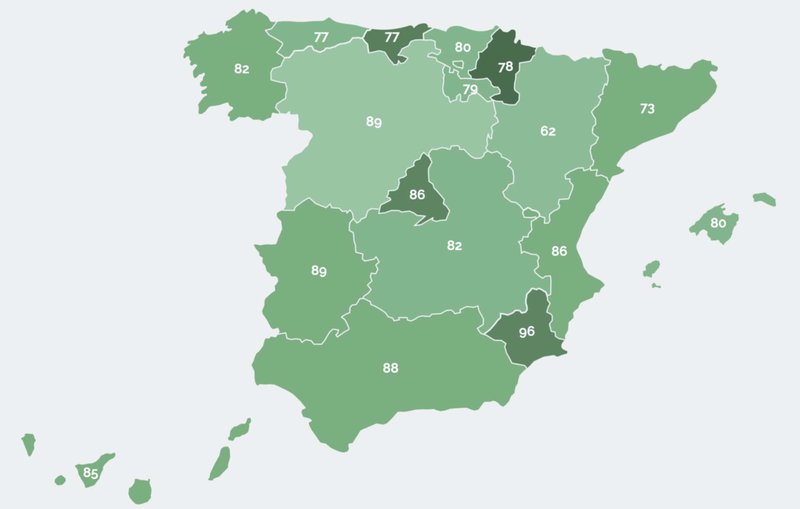

SMEs' Failed Payments

Although business delinquencies decreased during Q2 (2021), it was merely a marginal 3.8 percentage compared to the previous quarter, and by 2.4 percentage compared to the same period in 2020 (YoY).

More specifically, during the second quarter the general Average Payment Period (PMP) of Spanish companies reached 81 days (see below by region), a decrease of almost seven days compared to the previous period, which was the worst quarter since 2013.

These delays erode the ability for these companies to face payments themselves, which is compromising their financial liquidity and so their competitiveness likewise.

According to the report, delinquencies have increased in sectors such as construction with 101.1 days on average, textile industry 88.3, and plastics with 84.3 days.

Other industries have 'better' payment terms, which are still very high overall, this is the case of food distribution, which has an average payment of 64.9 days.

Needless to say that the resilience of the banking and financing sector has been a critical leverage enabling these organisations to sustain their operations.

However, as pointed by the OECD in their report SME and Entrepreneurship Outlook 2021, lower production, lower wages and lower profits could lead to increased default rates by consumers and businesses by equal, which in turn could contribute to increasing debt, defaults on mortgages and downward pressure on real estate prices too.

Taken together, depressed economic conditions and rising delinquency payments will lead to non-performing loans, combined could weaken the loss absorption capacities of already exhausted banks.

Despite the fact that the industry grew smoothly on the second quarter, capital investment (especially in the construction sector) has not recovered from the retrenchment in the first quarter, and has already seen three consecutive quarters in decline.

By means of reference, the construction sector was set to have the highest share of non-performing loans (NPLs), with their NPL ratio standing at 9.5% by September 2020.

Culture, Credit and Debt

Although some might disagree, I believe the high delinquency rate is very much influenced not only by the current dynamics of financial instability, but more generally by a cultural problem, an endemic one.

More broadly speaking, Spaniards have a collective reckless attitude towards debt, or as we say here, it's the often glorified ‘national picaresque’.

This recklessness not only emerges at a personal level, but as with culture, it has indeed extended its influence and normalisation through the business life too.

It remains unclear at this point how much of these deferred payments will end up as defaults.

In Spain, it is not custom that SMEs report unpaid invoices to the debt collection and credit rating agencies, which makes it really complex to assess the overall level of defaults.

However, the Bank of Spain has been warning of the threat for months.

At the end of last summer, the Bank of Spain published a report on the liquidity needs and solvency of non-financial companies after the outbreak of the Coronavirus crisis.

The document estimated that between 30% and 32% of Spanish companies already had a high probability of default, a figure that rises above 50% in the case of small companies.

As a side note, let's remember that payment delinquency does not refers to payment default, it refers to the deferment (postponement) of liabilities such as invoices.